![[Class 11] Expense Paid, Expense Outstanding & Expense Paid in Advance - Chapter 5 - Accounting Equation](https://cdn.teachoo.com/a72f5b7e-e038-4c6e-bcde-f59056b17b6a/slide-1-expense-paid-expense-outstanding-and-expense-paid-in-advance-in-accounting-equation.jpg)

Chapter 5 - Accounting Equation

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

Last updated at February 25, 2026 by Teachoo

Transcript

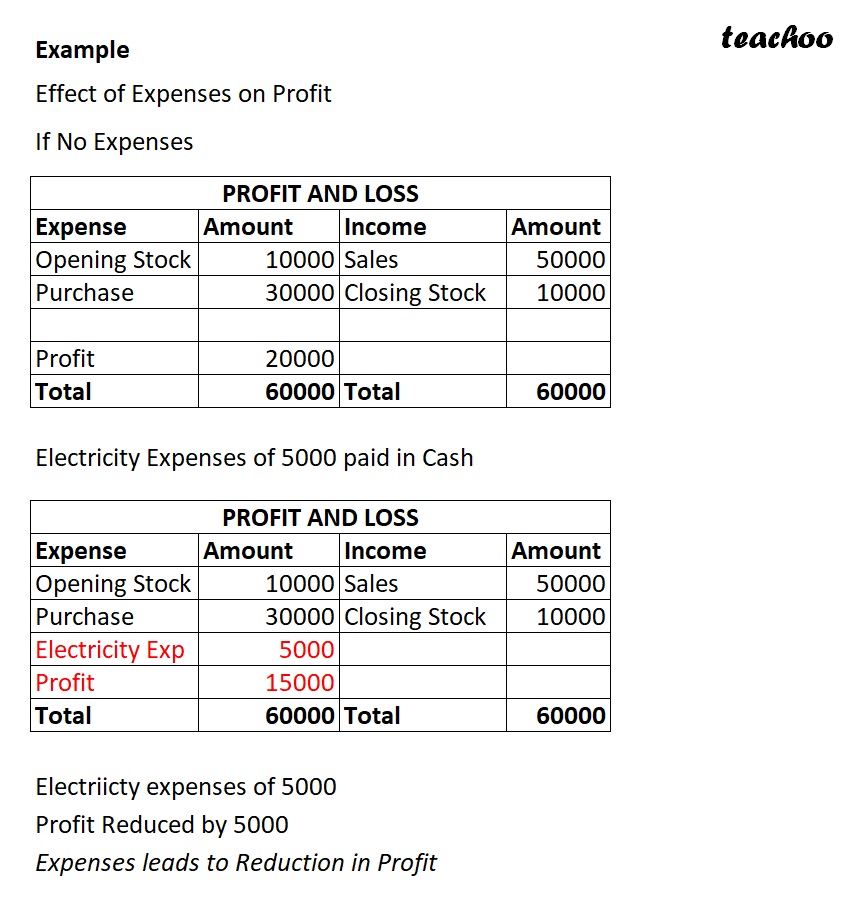

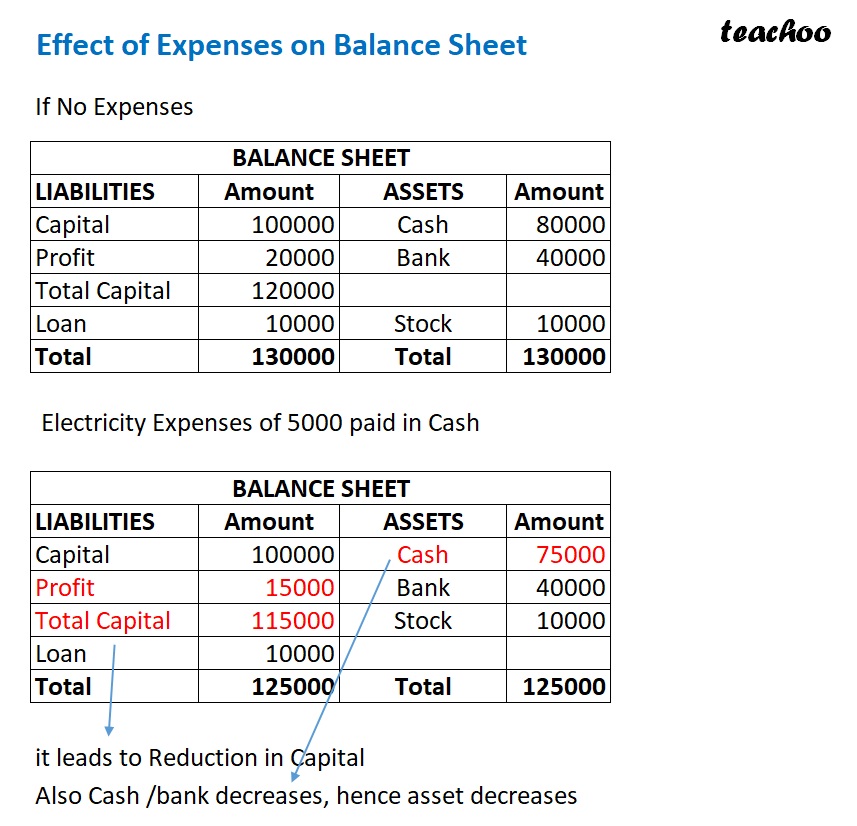

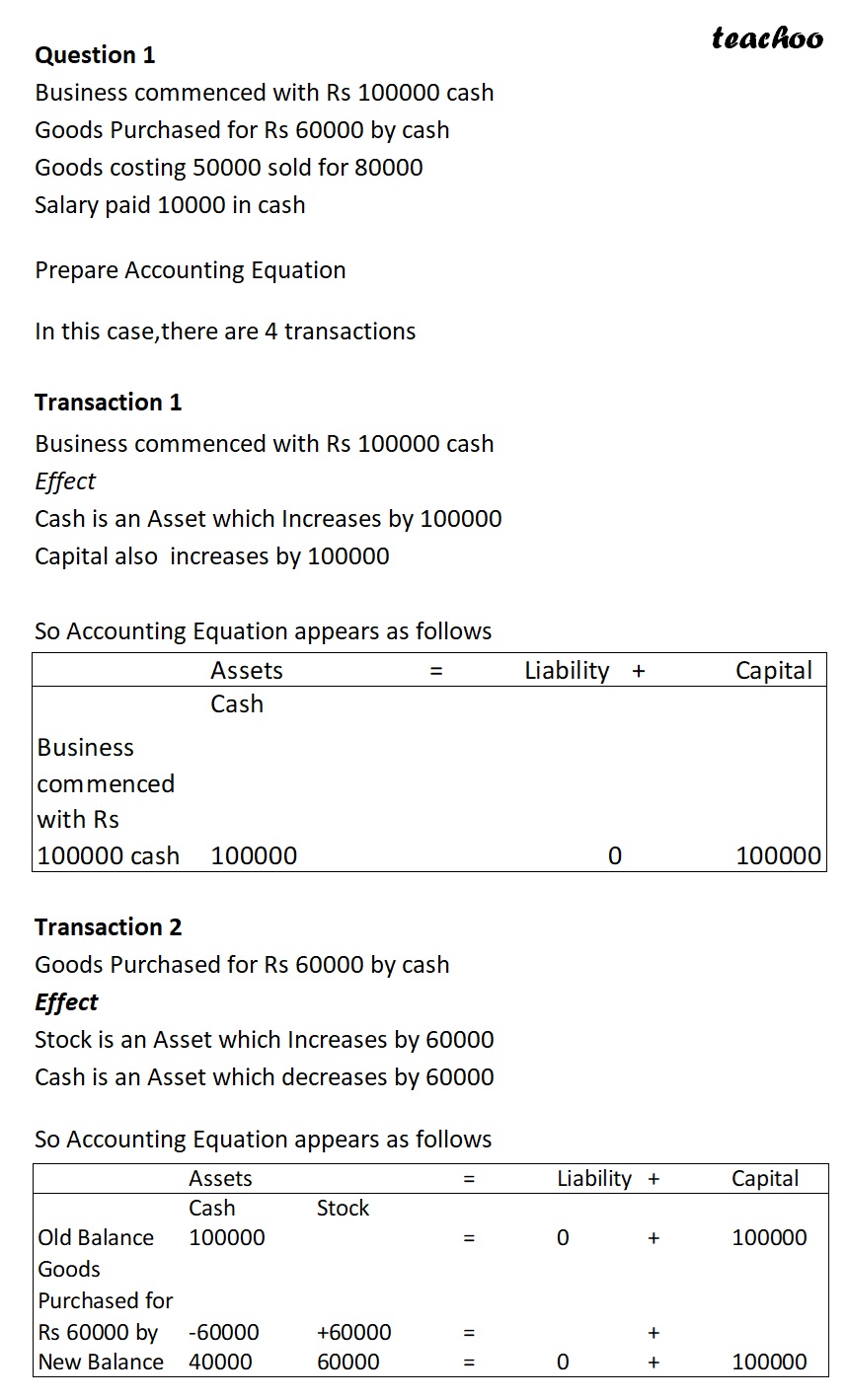

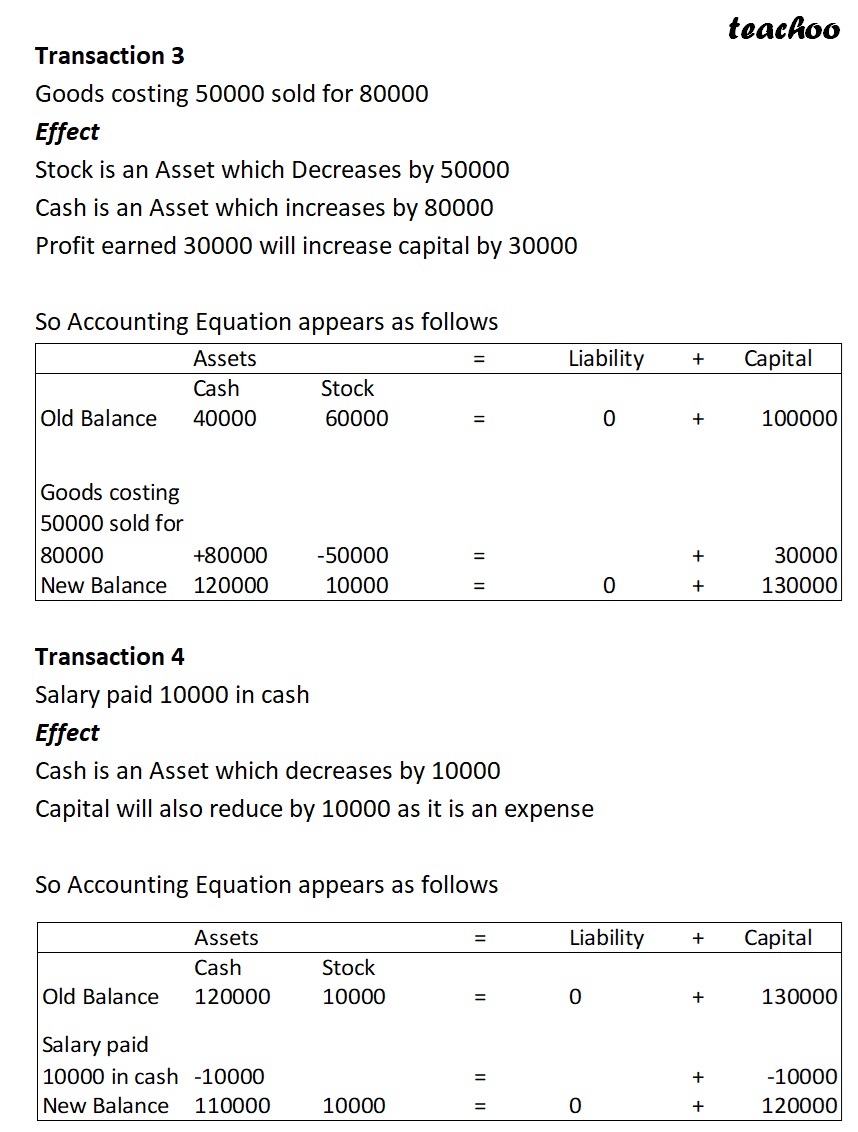

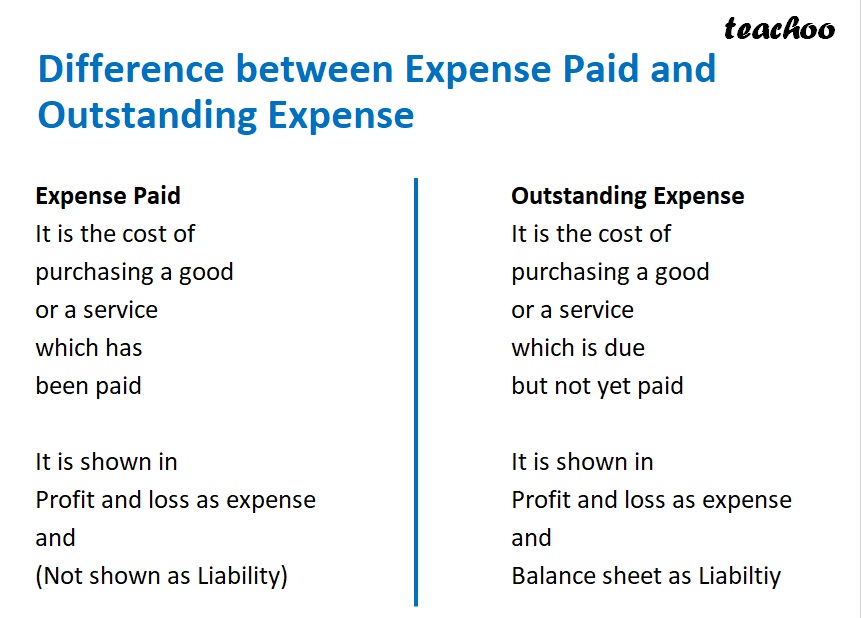

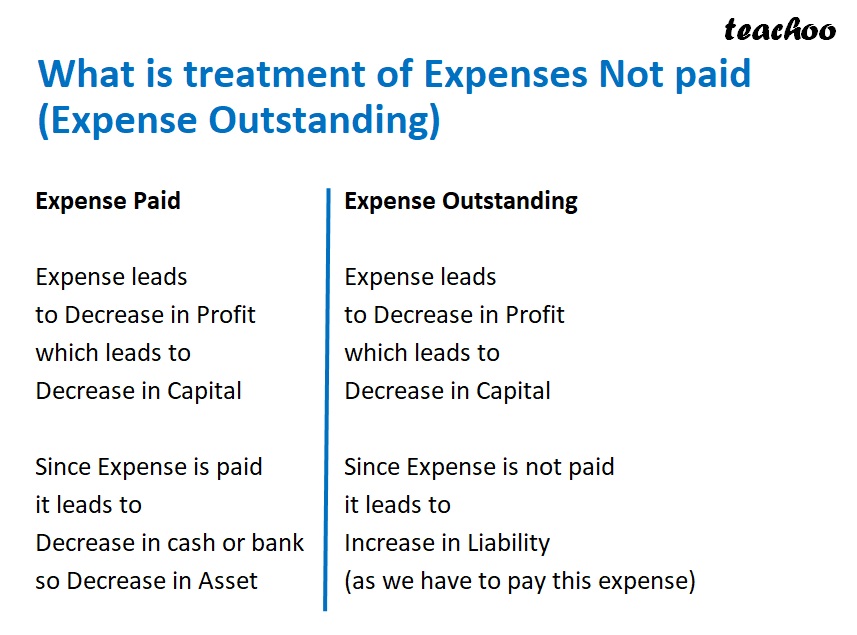

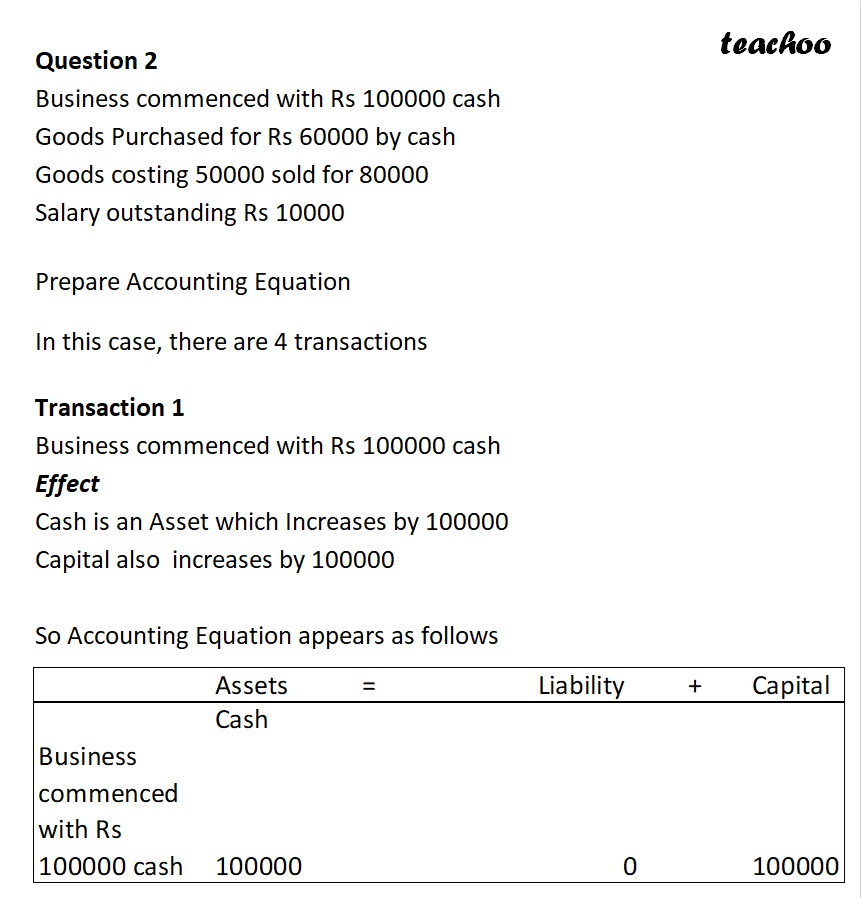

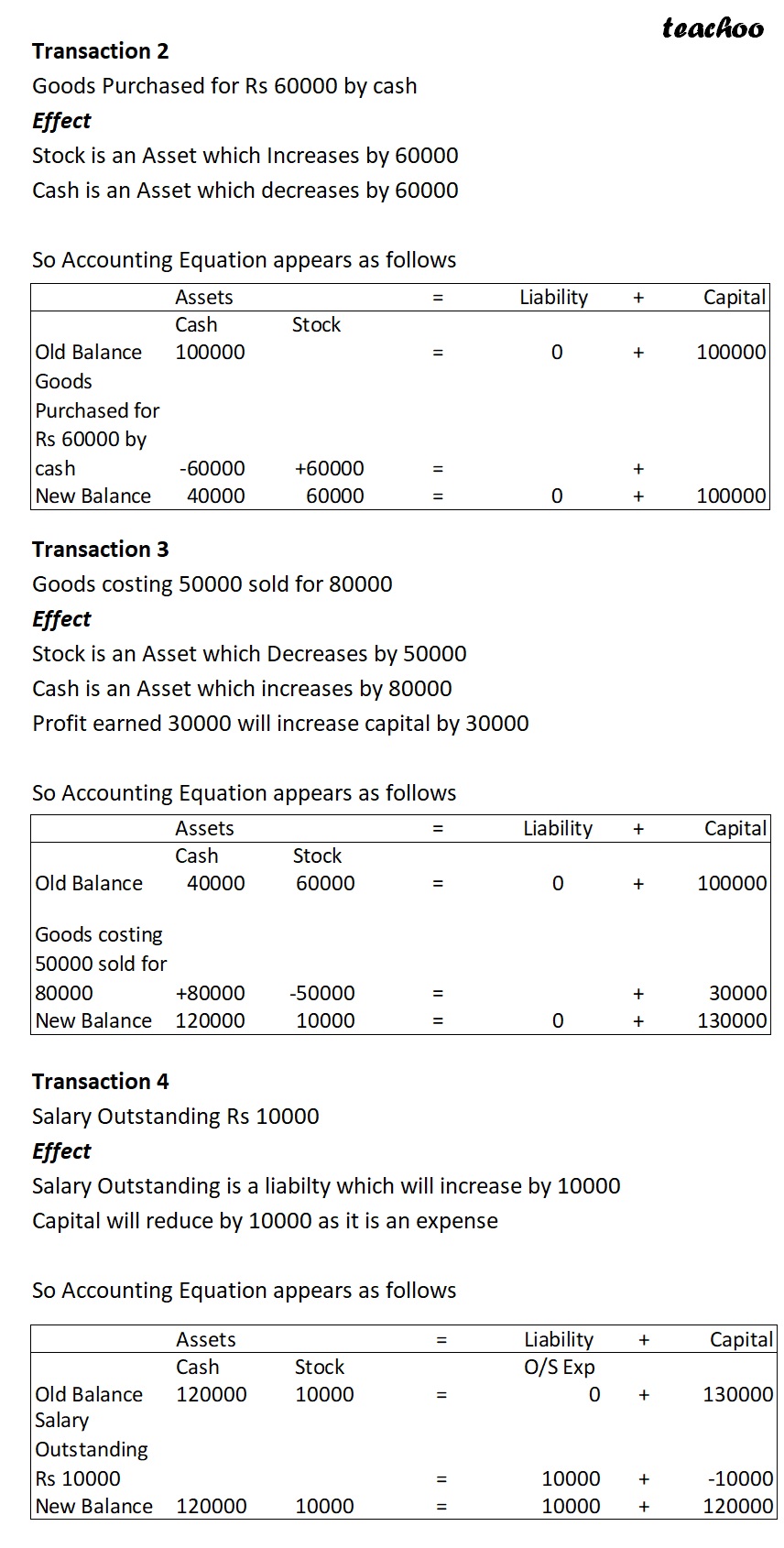

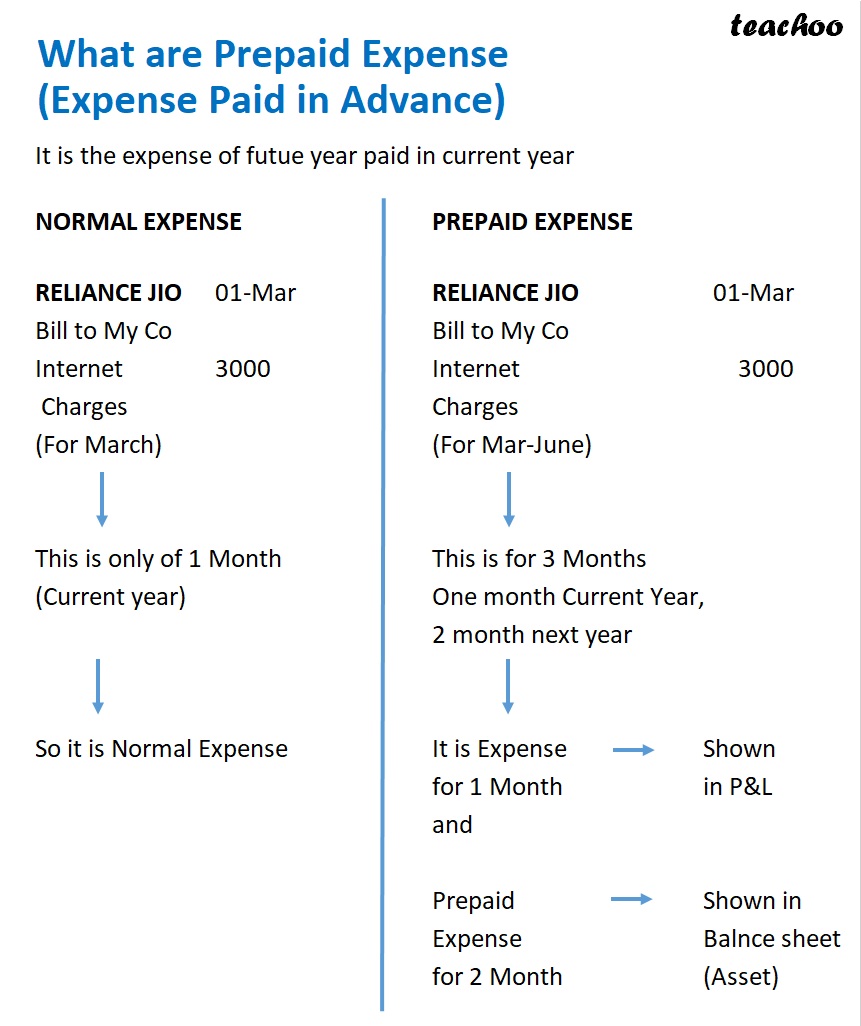

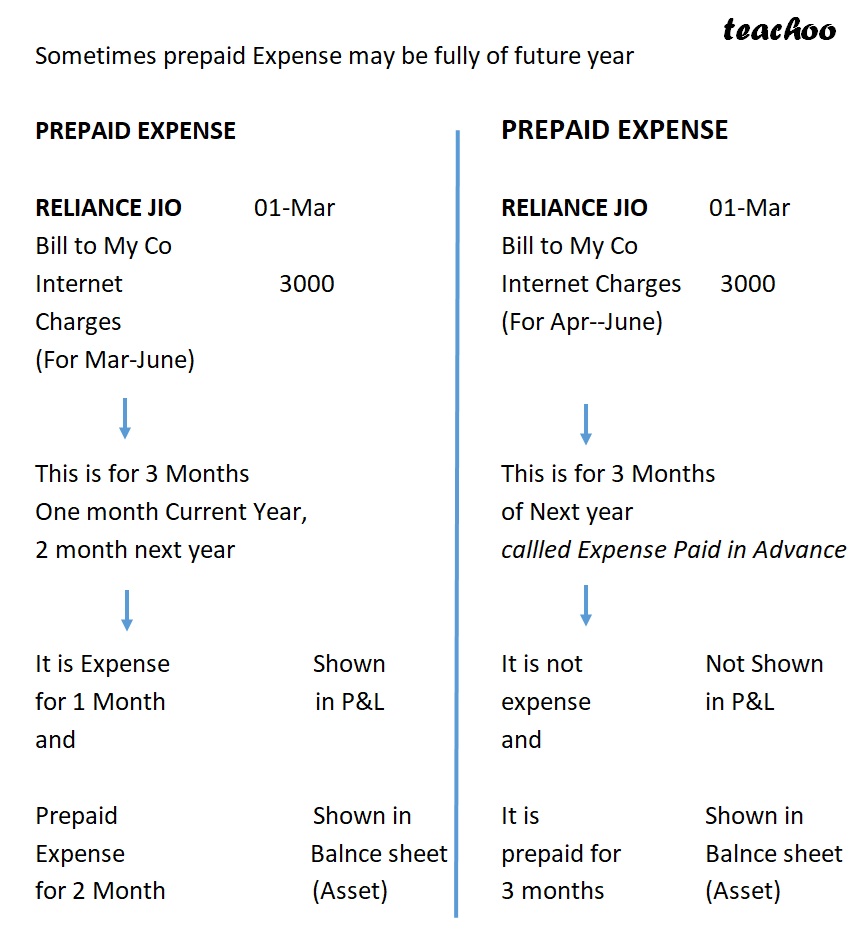

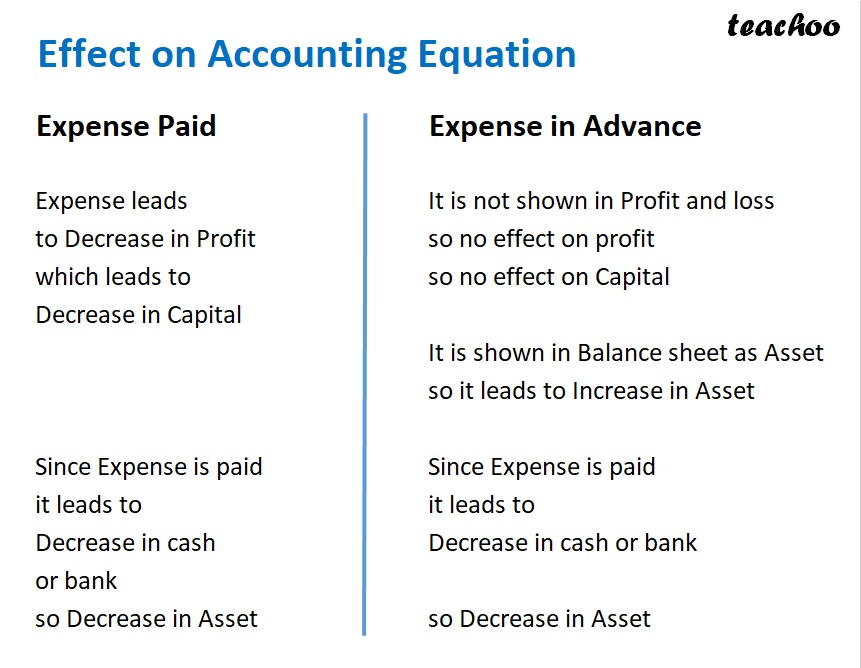

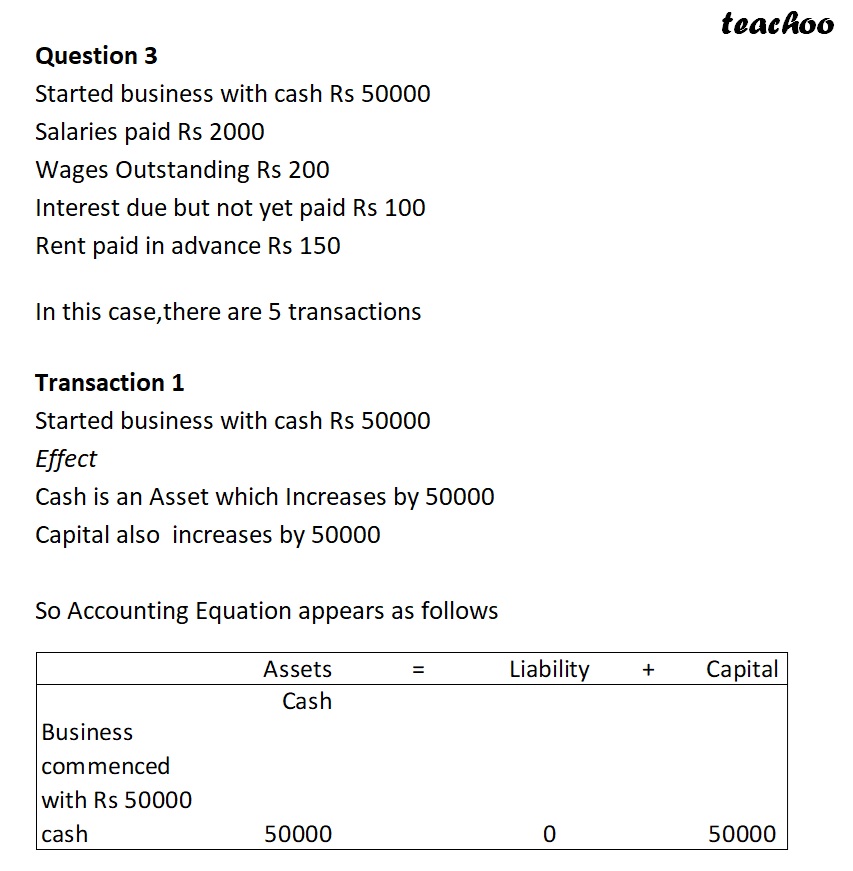

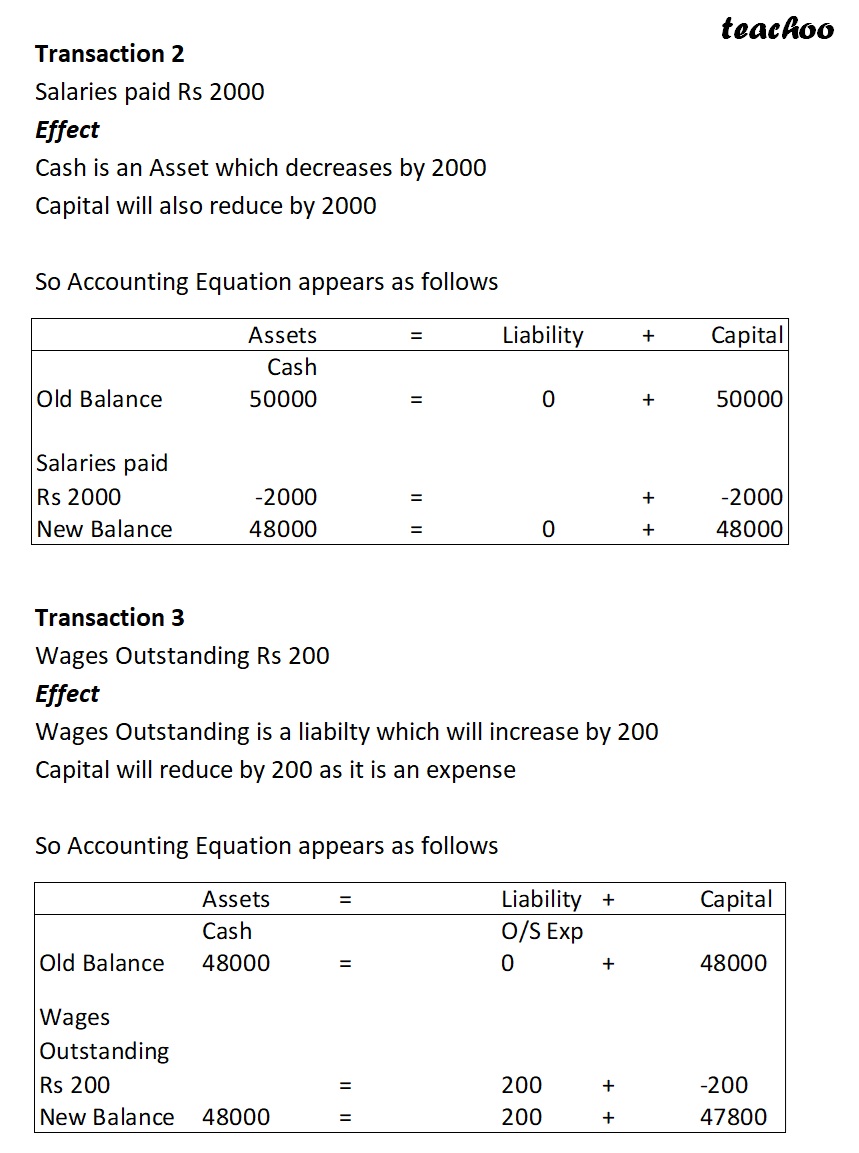

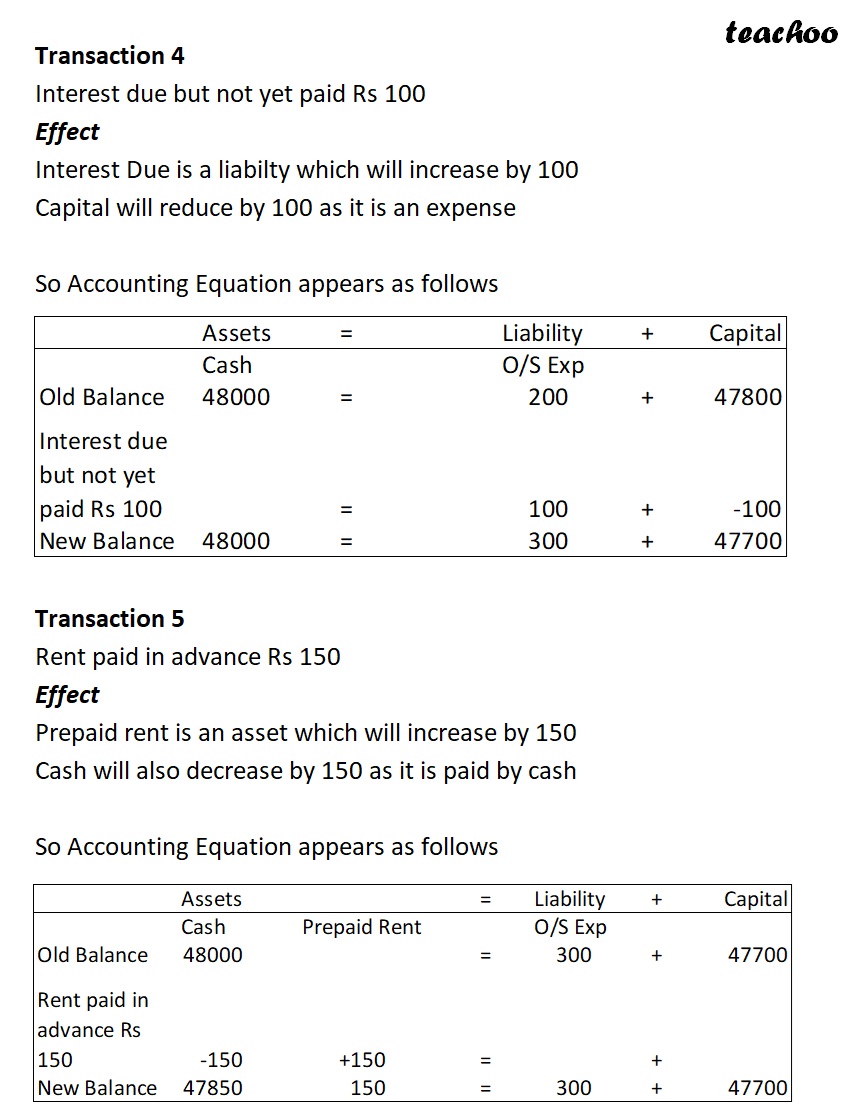

Expense Paid,Expense Outstanding and Expense Paid in Advance in Accounting Equation What is Effect of Expenses on Profit Expenses leads to Reduction in Profit More the expenses,less the profit What is Effect of Expenses on Balalnce sheet We know that Profit is added to capital Because of expenses,Profit Reduces Due to this ,capital also reduces Also ,if Expenses are paid in cash,it leads to decrease in cash Since cash is an asset,it cause decrease in assets Example Effect of Expenses on Profit If No Expenses PROFIT AND LOSS Expense Amount Income Amount Opening Stock 10000 Sales 50000 Purchase 30000 Closing Stock 10000 Profit 20000 Total 60000 Total 60000 Electricity Expenses of 5000 paid in Cash PROFIT AND LOSS Expense Amount Income Amount Opening Stock 10000 Sales 50000 Purchase 30000 Closing Stock 10000 Electricity Exp 5000 Profit 15000 Total 60000 Total 60000 Electriicty expenses of 5000 Profit Reduced by 5000 Expenses leads to Reduction in Profit Effect of Expenses on Balance Sheet If No Expenses BALANCE SHEET LIABILITIES Amount ASSETS Amount Capital 100000 Cash 80000 Profit 20000 Bank 40000 Total Capital 120000 Loan 10000 Stock 10000 Total 130000 Total 130000 Electricity Expenses of 5000 paid in Cash BALANCE SHEET LIABILITIES Amount ASSETS Amount Capital 100000 Cash 75000 Profit 15000 Bank 40000 Total Capital 115000 Stock 10000 Loan 10000 Total 125000 Total 125000 it leads to Reduction in Capital Also Cash /bank decreases,hence asset decreases Question 1 Business commenced with Rs 100000 cash Goods Purchased for Rs 60000 by cash Goods costing 50000 sold for 80000 Salary paid 10000 in cash Prepare Accounting Equation In this case,there are 4 transactions Transaction 1 Business commenced with Rs 100000 cash Effect Cash is an Asset which Increases by 100000 Capital also increases by 100000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Business commenced with Rs 100000 cash 100000 0 100000 Transaction 2 Goods Purchased for Rs 60000 by cash Effect Stock is an Asset which Increases by 60000 Cash is an Asset which decreases by 60000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Stock Old Balance 100000 = 0 + 100000 Goods Purchased for Rs 60000 by cash -60000 +60000 = + New Balance 40000 60000 = 0 + 100000 Transaction 3 Goods costing 50000 sold for 80000 Effect Stock is an Asset which Decreases by 50000 Cash is an Asset which increases by 80000 Profit earned 30000 will increase capital by 30000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Stock Old Balance 40000 60000 = 0 + 100000 Goods costing 50000 sold for 80000 +80000 -50000 = + 30000 New Balance 120000 10000 = 0 + 130000 Transaction 4 Salary paid 10000 in cash Effect Cash is an Asset which decreases by 10000 Capital will also reduce by 10000 as it is an expense So Accounting Equation appears as follows Assets = Liability + Capital Cash Stock Old Balance 120000 10000 = 0 + 130000 Salary paid 10000 in cash -10000 = + -10000 New Balance 110000 10000 = 0 + 120000 Difference between Expense Paid and Outstanding Expense Expense Paid Outstanding Expense It is the cost of It is the cost of purchasing a good purchasing a good or a service or a service which has which is due been paid but not yet paid It is shown in It is shown in Profit and loss as expense Profit and loss as expense and and (Not shown as Liability) Balance sheet as Liabiltiy What is treatment of Expenses Not paid (Expense Outstanding) Expense Paid Expense Outstanding Expense leads Expense leads to Decrease in Profit to Decrease in Profit which leads to which leads to Decrease in Capital Decrease in Capital Since Expense is paid Since Expense is not paid it leads to it leads to Decrease in cash or bank Increase in Liability so Decrease in Asset (as we have to pay this expense) Question 2 Business commenced with Rs 100000 cash Goods Purchased for Rs 60000 by cash Goods costing 50000 sold for 80000 Salary outstanding Rs 10000 Prepare Accounting Equation In this case,there are 4 transactions Transaction 1 Business commenced with Rs 100000 cash Effect Cash is an Asset which Increases by 100000 Capital also increases by 100000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Business commenced with Rs 100000 cash 100000 0 100000 Transaction 2 Goods Purchased for Rs 60000 by cash Effect Stock is an Asset which Increases by 60000 Cash is an Asset which decreases by 60000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Stock Old Balance 100000 = 0 + 100000 Goods Purchased for Rs 60000 by cash -60000 +60000 = + New Balance 40000 60000 = 0 + 100000 Transaction 3 Goods costing 50000 sold for 80000 Effect Stock is an Asset which Decreases by 50000 Cash is an Asset which increases by 80000 Profit earned 30000 will increase capital by 30000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Stock Old Balance 40000 60000 = 0 + 100000 Goods costing 50000 sold for 80000 +80000 -50000 = + 30000 New Balance 120000 10000 = 0 + 130000 Transaction 4 Salary Outstanding Rs 10000 Effect Salary Outstanding is a liabilty which will increase by 10000 Capital will reduce by 10000 as it is an expense So Accounting Equation appears as follows Assets = Liability + Capital Cash Stock O/S Exp Old Balance 120000 10000 = 0 + 130000 Salary Outstanding Rs 10000 = 10000 + -10000 New Balance 120000 10000 = 10000 + 120000 What are Prepaid Expense (Expense Paid in Advance) It is the expense of futue year paid in current year NORMAL EXPENSE PREPAID EXPENSE RELIANCE JIO 01-Mar RELIANCE JIO 01-Mar Bill to My Co Bill to My Co Internet 3000 Internet 3000 Charges Charges (For March) (For Mar-June) I I This is only of 1 Month This is for 3 Months (Current year) One month Current Year,2 month next year I I So it is Normal Expense It is Expense --> Shown in P&L for 1 Month and Prepaid Expense --> Shown in Balnce sheet for 2 Month (Asset) Sometimes prepaid Expense may be fully of future year PREPAID EXPENSE PREPAID EXPENSE RELIANCE JIO 01-Mar RELIANCE JIO 01-Mar Bill to My Co Bill to My Co Internet 3000 Internet Charges 3000 Charges (For Apr--June) (For Mar-June) I I This is for 3 Months This is for 3 Months One month Current Year,2 month next year of Next year callled Expense Paid in Advance I I It is Expense --> Shown in P&L It is not expense --> Not Shown in P&L for 1 Month and and Prepaid --> Shown in Balnce sheet It is prepaid for --> Shown in Balnce sheet Expense (Asset) 3 months (Asset) for 2 Month Effect on Accounting Equation Expense Paid Expense in Advance Expense leads It is not shown in Profit and loss to Decrease in Profit so no effect on profit which leads to so no effect on Capital Decrease in Capital It is shown in Balance sheet as Asset so it leads to Increase in Asset Since Expense is paid Since Expense is paid it leads to it leads to Decrease in cash Decrease in cash or bank or bank so Decrease in Asset so Decrease in Asset Question 3 Started business with cash Rs 50000 Salaries paid Rs 2000 Wages Outstanding Rs 200 Interest due but not yet paid Rs 100 Rent paid in advance Rs 150 In this case,there are 5 transactions Transaction 1 Started business with cash Rs 50000 Effect Cash is an Asset which Increases by 50000 Capital also increases by 50000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Business commenced with Rs 50000 cash 50000 0 50000 Transaction 2 Salaries paid Rs 2000 Effect Cash is an Asset which decreases by 2000 Capital will also reduce by 2000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Old Balance 50000 = 0 + 50000 Salaries paid Rs 2000 -2000 = + -2000 New Balance 48000 = 0 + 48000 Transaction 3 Wages Outstanding Rs 200 Effect Wages Outstanding is a liabilty which will increase by 200 Capital will reduce by 200 as it is an expense So Accounting Equation appears as follows Assets = Liability + Capital Cash O/S Exp Old Balance 48000 = 0 + 48000 Wages Outstanding Rs 200 = 200 + -200 New Balance 48000 = 200 + 47800 Transaction 4 Interest due but not yet paid Rs 100 Effect Interest Due is a liabilty which will increase by 100 Capital will reduce by 100 as it is an expense So Accounting Equation appears as follows Assets = Liability + Capital Cash O/S Exp Old Balance 48000 = 200 + 47800 Interest due but not yet paid Rs 100 = 100 + -100 New Balance 48000 = 300 + 47700 Transaction 5 Rent paid in advance Rs 150 Effect Prepaid rent is an asset which will increase by 150 Cash will also decrease by 150 as it is paid by cash So Accounting Equation appears as follows Assets = Liability + Capital Cash Prepaid Rent O/S Exp Old Balance 48000 = 300 + 47700 Rent paid in advance Rs 150 -150 +150 = + New Balance 47850 150 = 300 + 47700