Chapter 5 - Accounting Equation

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

Last updated at August 4, 2026 by Teachoo

Transcript

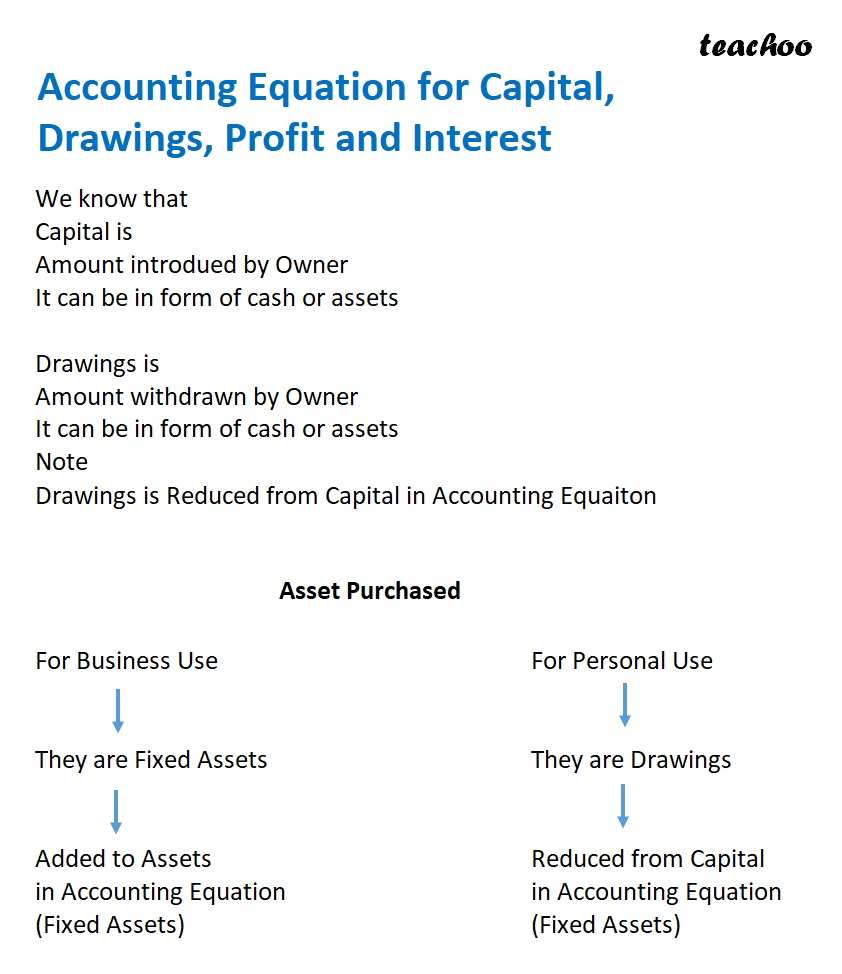

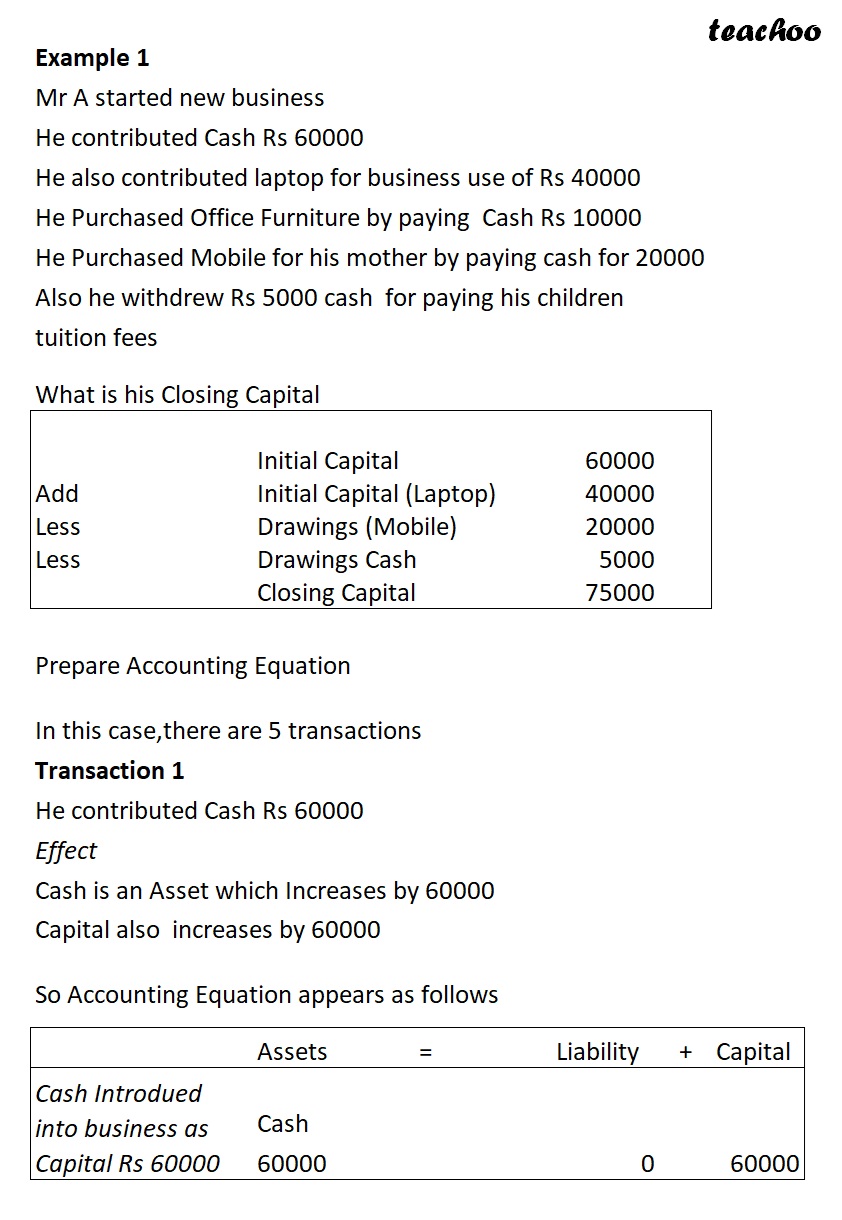

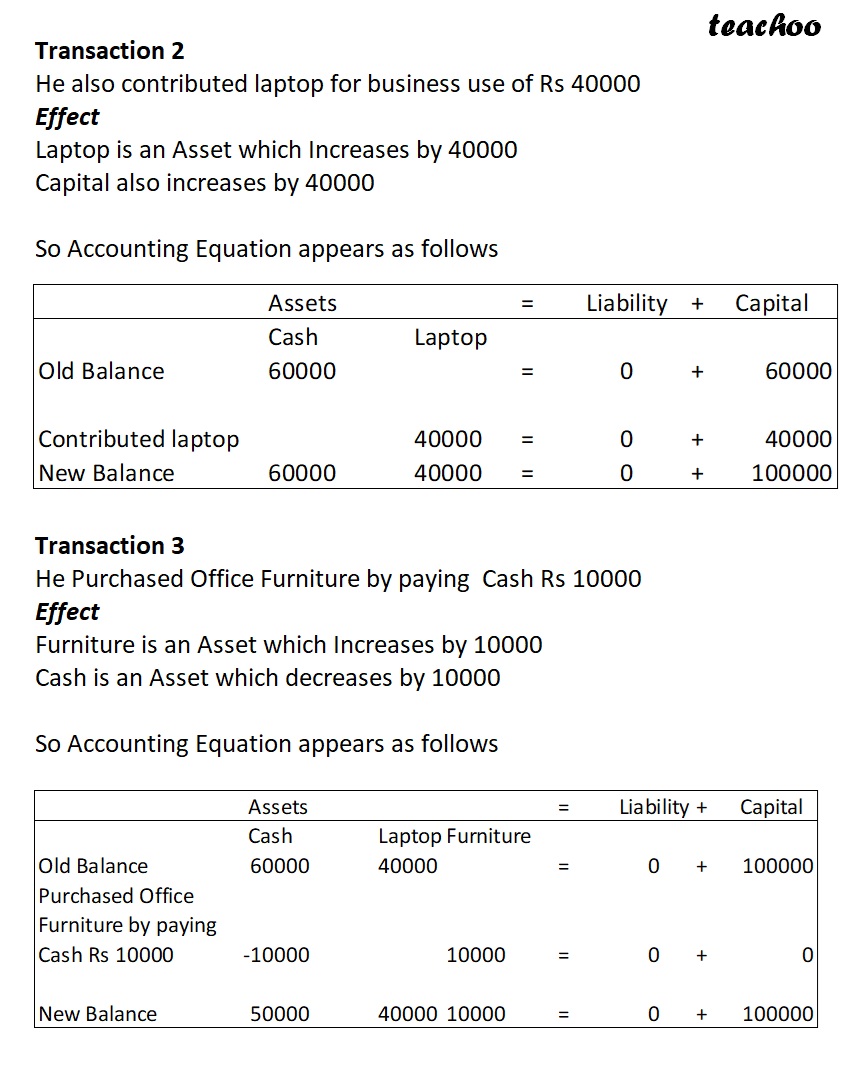

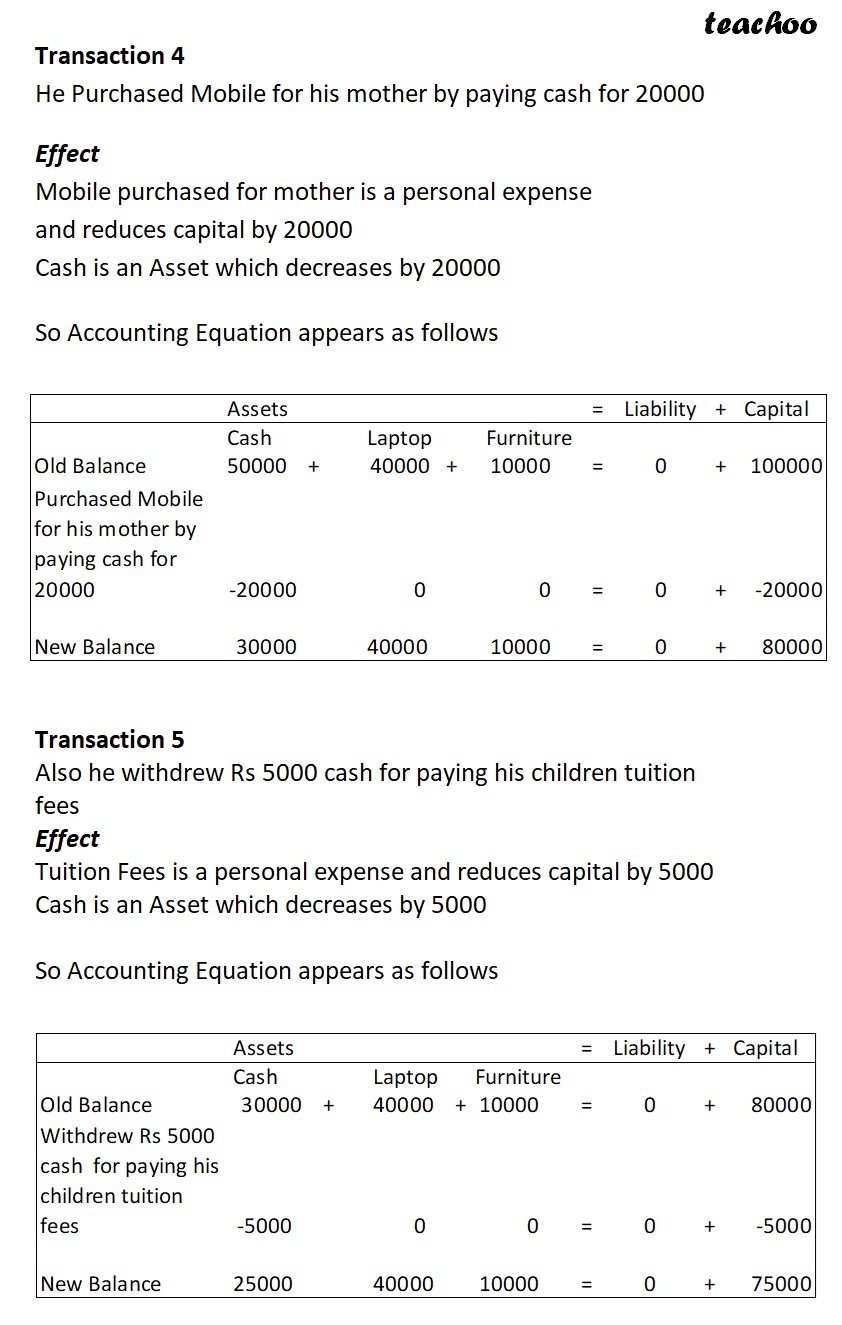

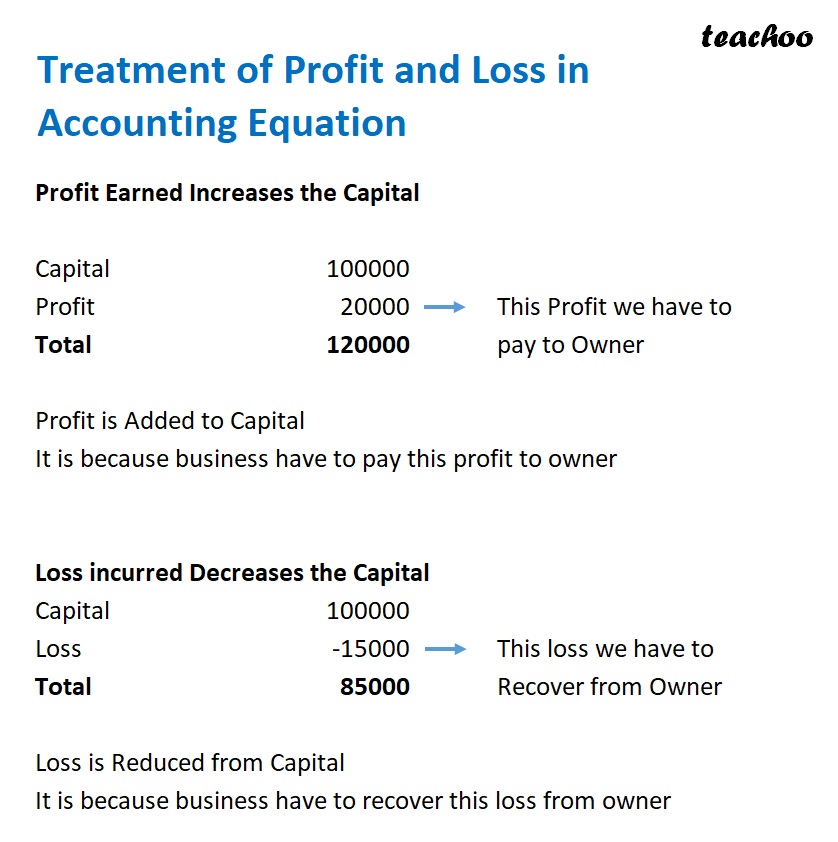

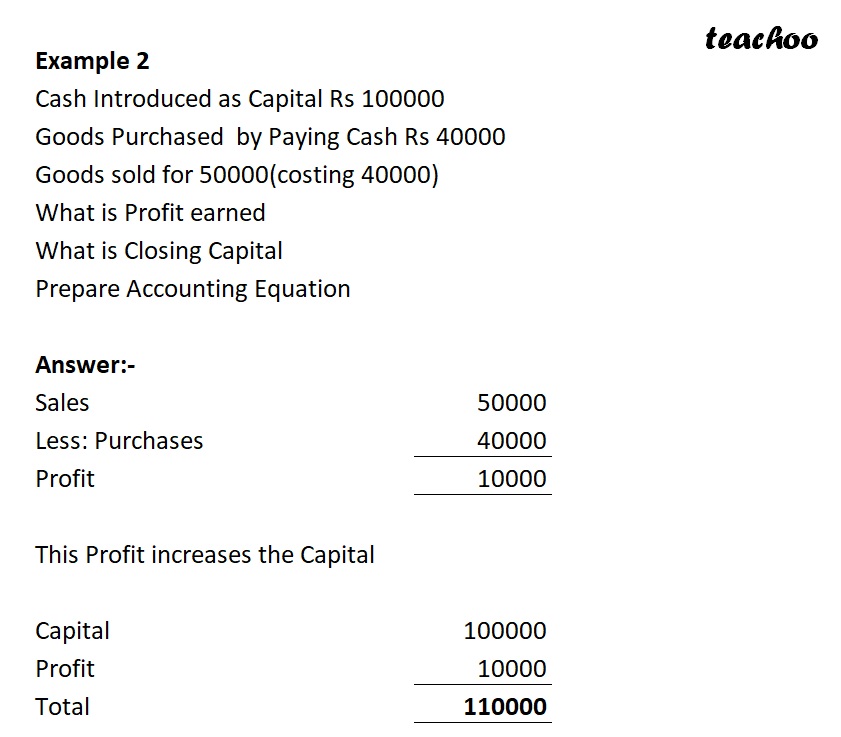

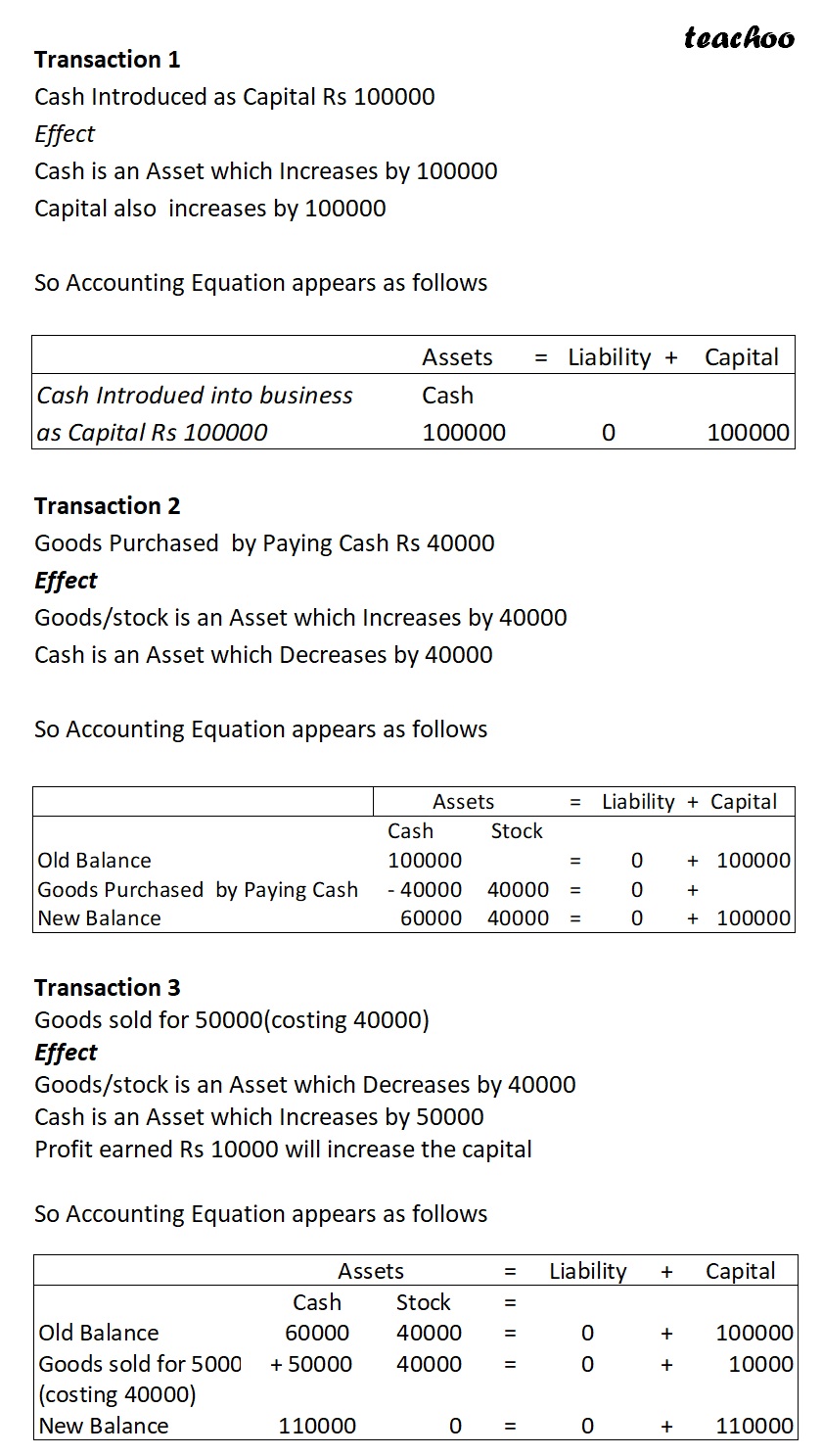

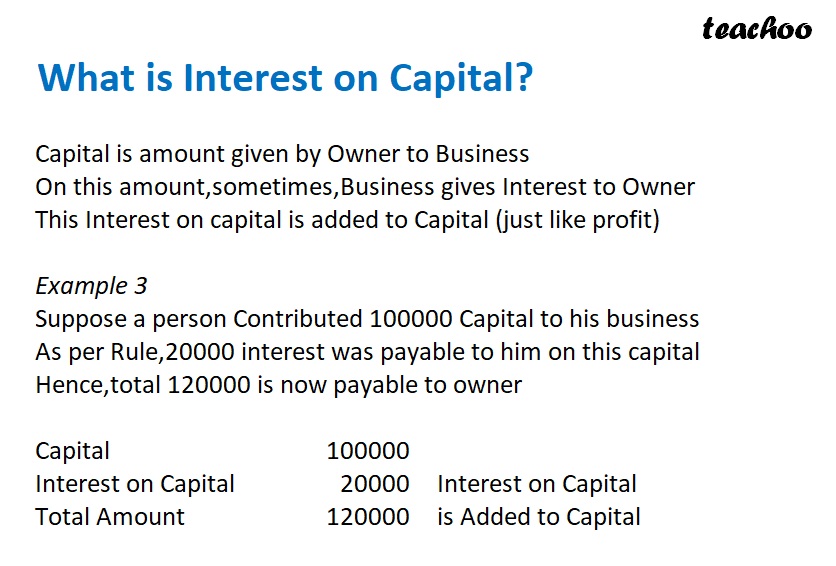

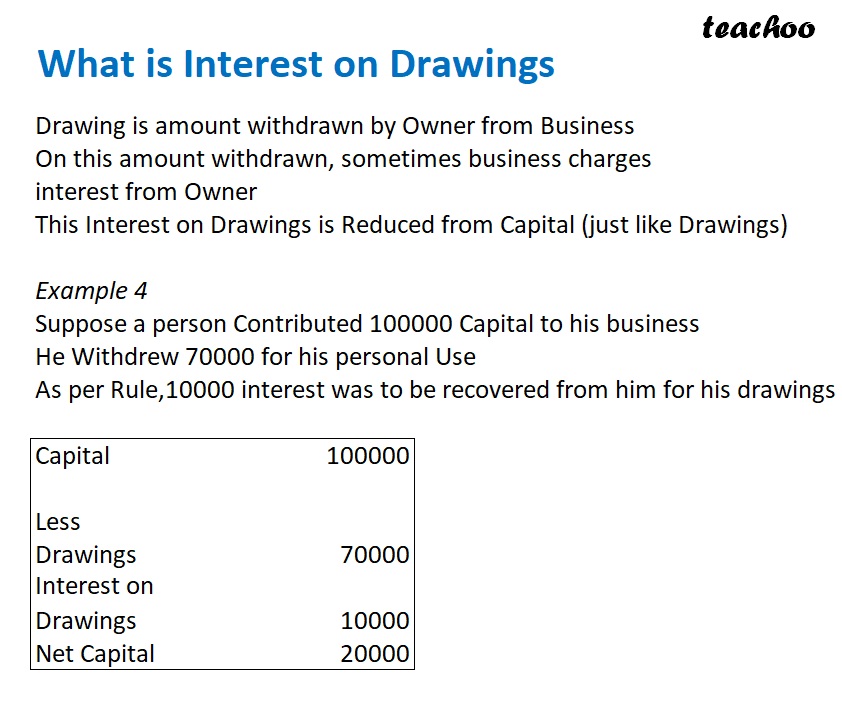

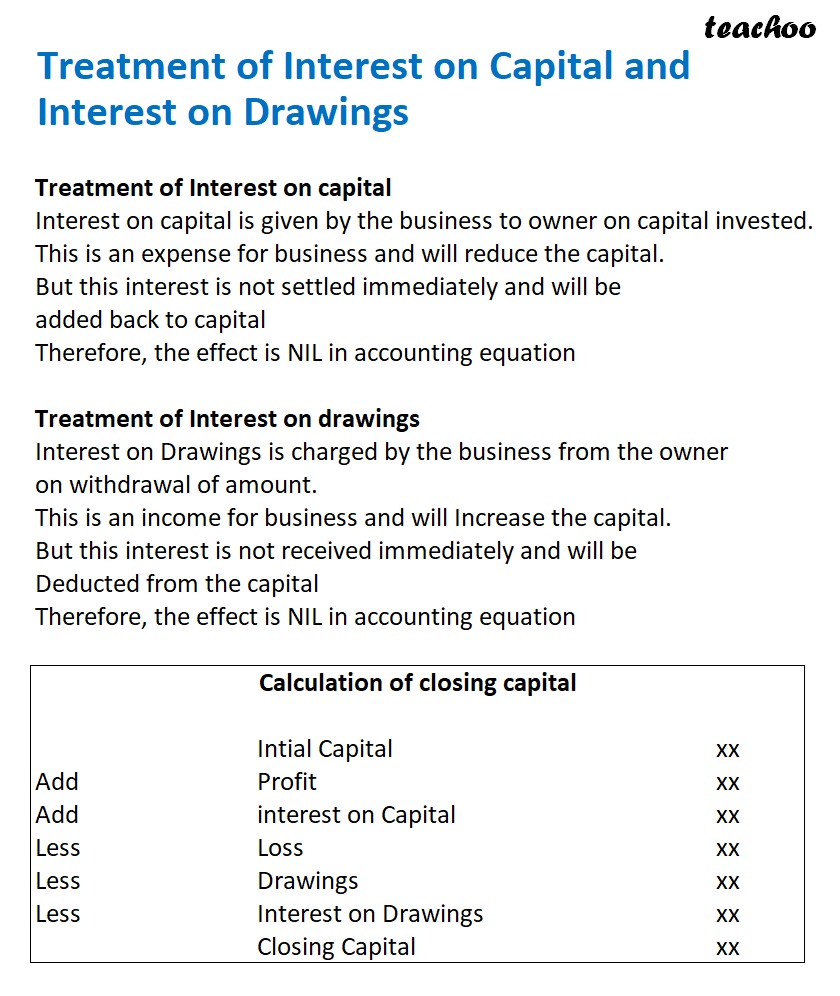

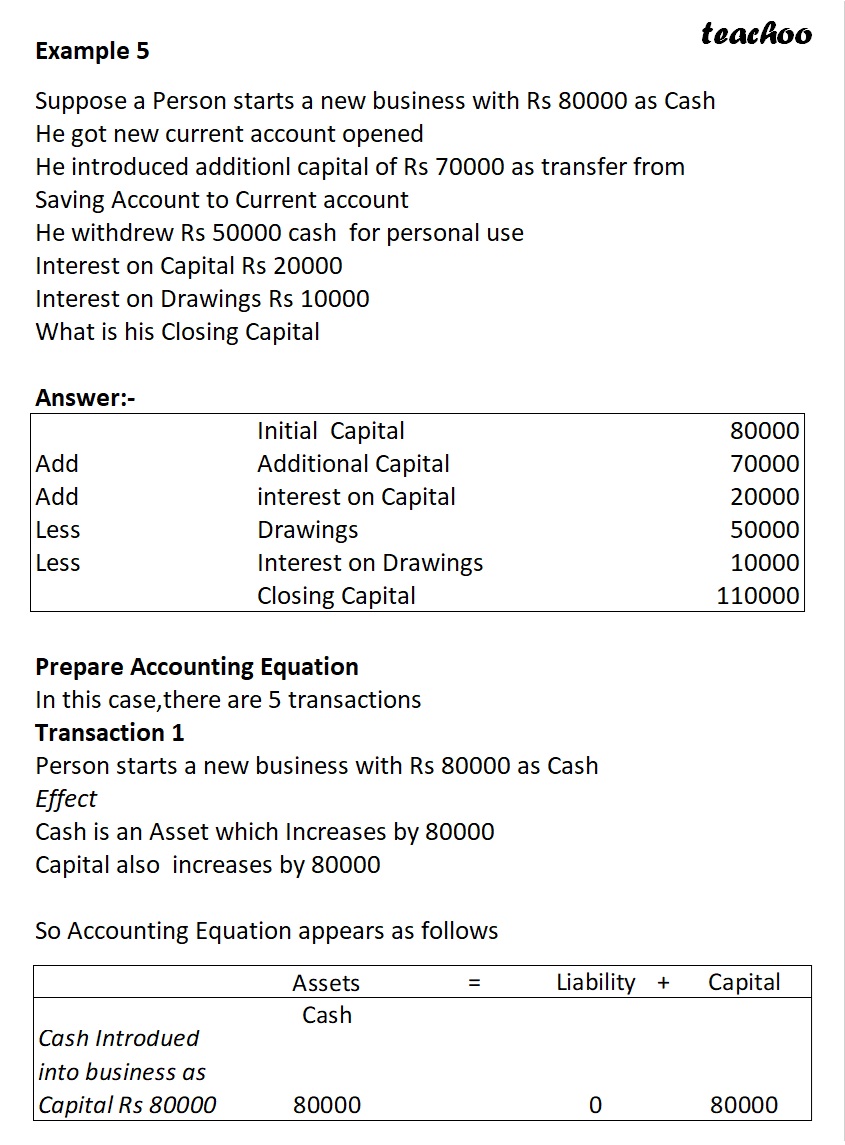

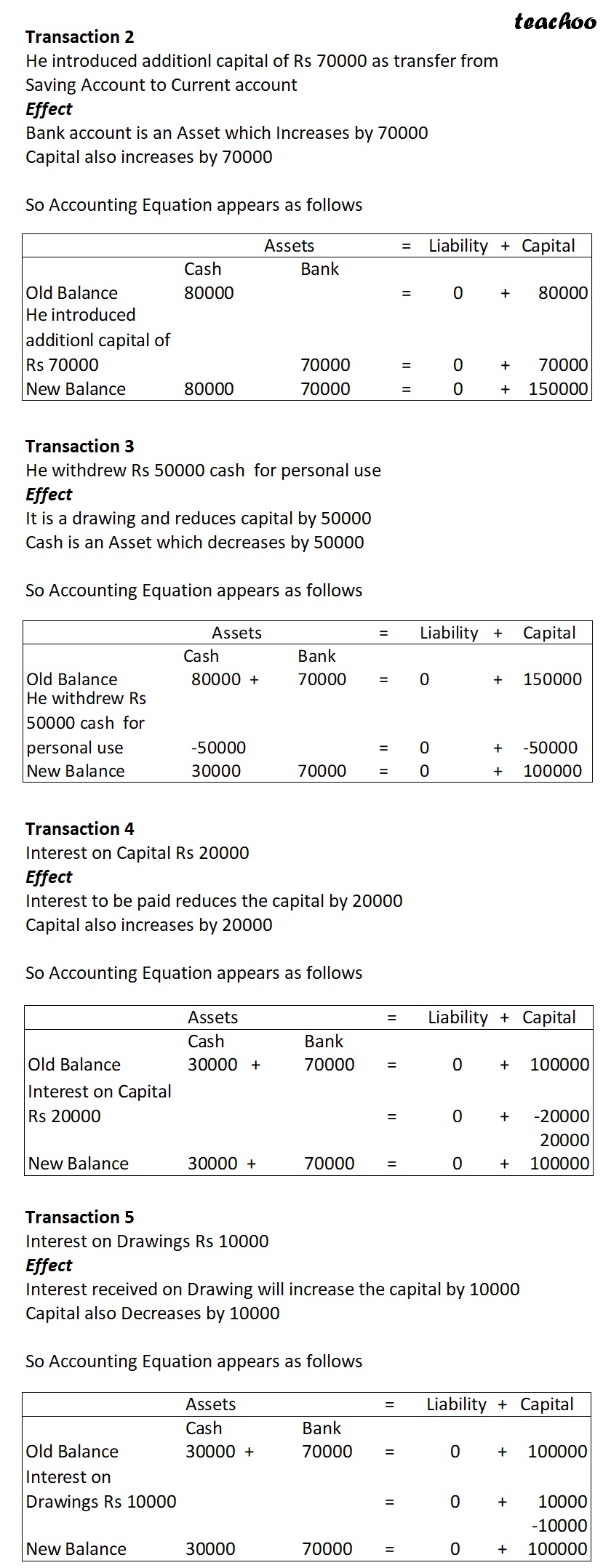

Accounting Equation for Capital, Drawings, Profit and Interest We know that Capital is Amount introdued by Owner It can be in form of cash or assets Drawings is Amount withdrawn by Owner It can be in form of cash or assets Note Drawings is Reduced from Capital in Accounting Equaiton Asset Purchased For Business Use For Personal Use They are Fixed Assets They are Drawings Added to Assets Reduced from Capital in Accounting Equation in Accounting Equation (Fixed Assets) (Fixed Assets) Example 1 Mr A started new business He contributed Cash Rs 60000 He also contributed laptop for business use of Rs 40000 He Purchased Office Furniture by paying Cash Rs 10000 He Purchased Mobile for his mother by paying cash for 20000 Also he withdrew Rs 5000 cash for paying his children tuition fees What is his Closing Capital Initial Capital 60000 Add Initial Capital (Laptop) 40000 Less Drawings (Mobile) 20000 Less Drawings Cash 5000 Closing Capital 75000 Prepare Accounting Equation In this case,there are 5 transactions Transaction 1 He contributed Cash Rs 60000 Effect Cash is an Asset which Increases by 60000 Capital also increases by 60000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Introdued into business as Capital Rs 60000 Cash 60000 0 60000 Transaction 2 He also contributed laptop for business use of Rs 40000 Effect Laptop is an Asset which Increases by 40000 Capital also increases by 40000 So Accounting Equation appears as follows Transaction 3 He Purchased Office Furniture by paying Cash Rs 10000 Effect Furniture is an Asset which Increases by 10000 Cash is an Asset which decreases by 10000 So Accounting Equation appears as follows Transaction 4 He Purchased Mobile for his mother by paying cash for 20000 Effect Mobile purchased for mother is a personal expense and reduces capital by 20000 Cash is an Asset which decreases by 20000 So Accounting Equation appears as follows Transaction 5 Also he withdrew Rs 5000 cash for paying his children tuition fees Effect Tuition Fees is a personal expense and reduces capital by 5000 Cash is an Asset which decreases by 5000 So Accounting Equation appears as follows Treatment of Profit and Loss in Accounting Equation Profit Earned Increases the Capital Capital 100000 Profit 20000 This Profit we have to Total 120000 pay to Owner Profit is Added to Capital It is because business have to pay this profit to owner Loss incurred Decreases the Capital Capital 100000 Loss -15000 This loss we have to Total 85000 Recover from Owner Loss is Reduced from Capital It is because business have to recover this loss from owner Example 2 Cash Introduced as Capital Rs 100000 Goods Purchased by Paying Cash Rs 40000 Goods sold for 50000(costing 40000) What is Profit earned What is Closing Capital Prepare Accounting Equation Answer:- Sales 50000 Less: Purchases 40000 Profit 10000 This Profit increases the Capital Capital 100000 Profit 10000 Total 110000 Transaction 1 Cash Introduced as Capital Rs 100000 Effect Cash is an Asset which Increases by 100000 Capital also increases by 100000 So Accounting Equation appears as follows Transaction 2 Goods Purchased by Paying Cash Rs 40000 Effect Goods/stock is an Asset which Increases by 40000 Cash is an Asset which Decreases by 40000 So Accounting Equation appears as follows Transaction 3 Goods sold for 50000(costing 40000) Effect Goods/stock is an Asset which Decreases by 40000 Cash is an Asset which Increases by 50000 Profit earned Rs 10000 will increase the capital So Accounting Equation appears as follows What is Interest on Capital? Capital is amount given by Owner to Business On this amount,sometimes,Business gives Interest to Owner This Interest on capital is added to Capital (just like profit) Example 3 Suppose a person Contributed 100000 Capital to his business As per Rule,20000 interest was payable to him on this capital Hence,total 120000 is now payable to owner Capital 100000 Interest on Capital 20000 Interest on Capital Total Amount 120000 is Added to Capital What is Interest on Drawings Drawing is amount withdrawn by Owner from Business On this amount withdrawn, sometimes business charges interest from Owner This Interest on Drawings is Reduced from Capital (just like Drawings) Example 4 Suppose a person Contributed 100000 Capital to his business He Withdrew 70000 for his personal Use As per Rule,10000 interest was to be recovered from him for his drawings Capital 100000 Less Drawings 70000 Interest on Drawings 10000 Net Capital 20000 Treatment of Interest on Capital and Interest on Drawings Treatment of Interest on capital Interest on capital is given by the business to owner on capital invested. This is an expense for business and will reduce the capital. But this interest is not settled immediately and will be added back to capital Therefore, the effect is NIL in accounting equation Treatment of Interest on drawings Interest on Drawings is charged by the business from the owner on withdrawal of amount. This is an income for business and will Increase the capital. But this interest is not received immediately and will be Deducted from the capital Therefore, the effect is NIL in accounting equation Calculation of closing capital Intial Capital xx Add Profit xx Add interest on Capital xx Less Loss xx Less Drawings xx Less Interest on Drawings xx Closing Capital xx Example 5 Suppose a Person starts a new business with Rs 80000 as Cash He got new current account opened He introduced additionl capital of Rs 70000 as transfer from Saving Account to Current account He withdrew Rs 50000 cash for personal use Interest on Capital Rs 20000 Interest on Drawings Rs 10000 What is his Closing Capital Answer:- Initial Capital 80000 Add Additional Capital 70000 Add interest on Capital 20000 Less Drawings 50000 Less Interest on Drawings 10000 Closing Capital 110000 Prepare Accounting Equation In this case,there are 5 transactions Transaction 1 Person starts a new business with Rs 80000 as Cash Effect Cash is an Asset which Increases by 80000 Capital also increases by 80000 So Accounting Equation appears as follows Transaction 2 He introduced additionl capital of Rs 70000 as transfer from Saving Account to Current account Effect Bank account is an Asset which Increases by 70000 Capital also increases by 70000 So Accounting Equation appears as follows Transaction 3 He withdrew Rs 50000 cash for personal use Effect It is a drawing and reduces capital by 50000 Cash is an Asset which decreases by 50000 So Accounting Equation appears as follows Transaction 4 Interest on Capital Rs 20000 Effect Interest to be paid reduces the capital by 20000 Capital also increases by 20000 So Accounting Equation appears as follows Transaction 5 Interest on Drawings Rs 10000 Effect Interest received on Drawing will increase the capital by 10000 Capital also Decreases by 10000 So Accounting Equation appears as follows