![Accounting Equation for Purchases, Sales, & Stock [Class 11 TS Grewal] - Chapter 5 - Accounting Equation](https://cdn.teachoo.com/2cadca36-e89d-4895-a78b-0c4c856c2f90/slide1-accounting-equation-for-purchase-sales-and-stock.jpg)

Chapter 5 - Accounting Equation

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

Last updated at February 23, 2026 by Teachoo

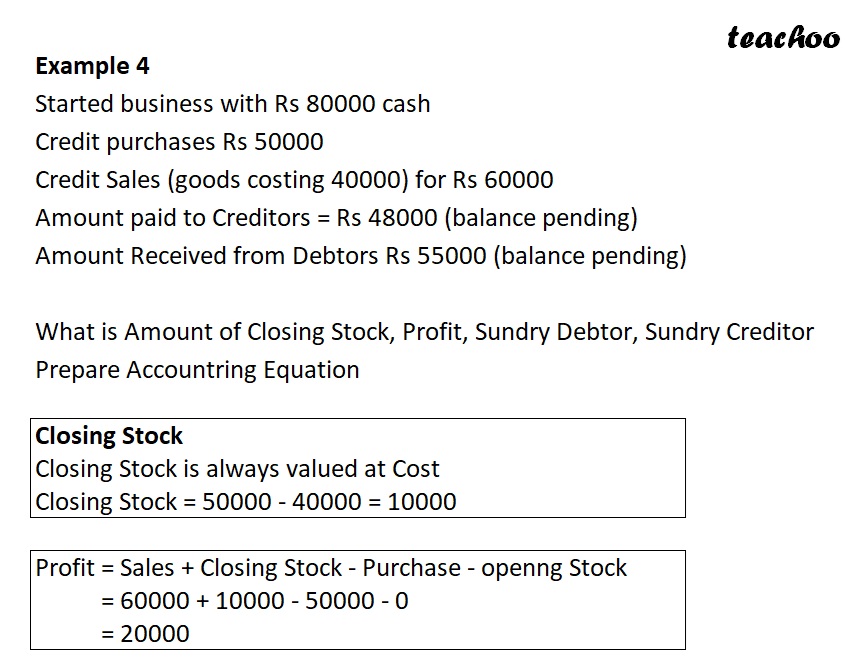

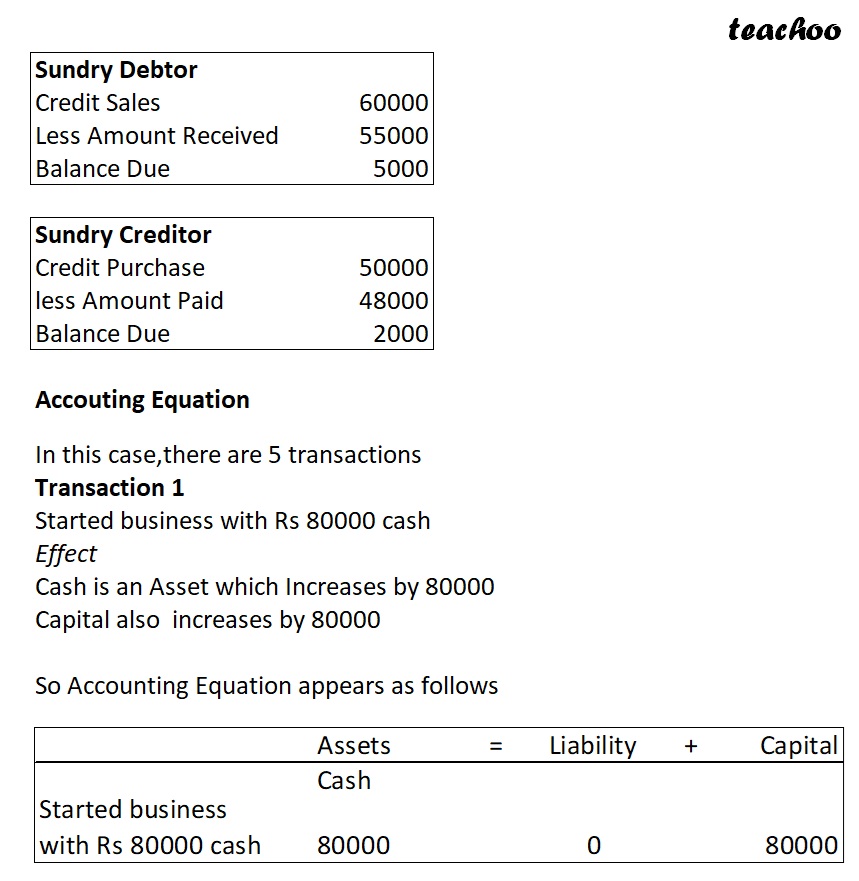

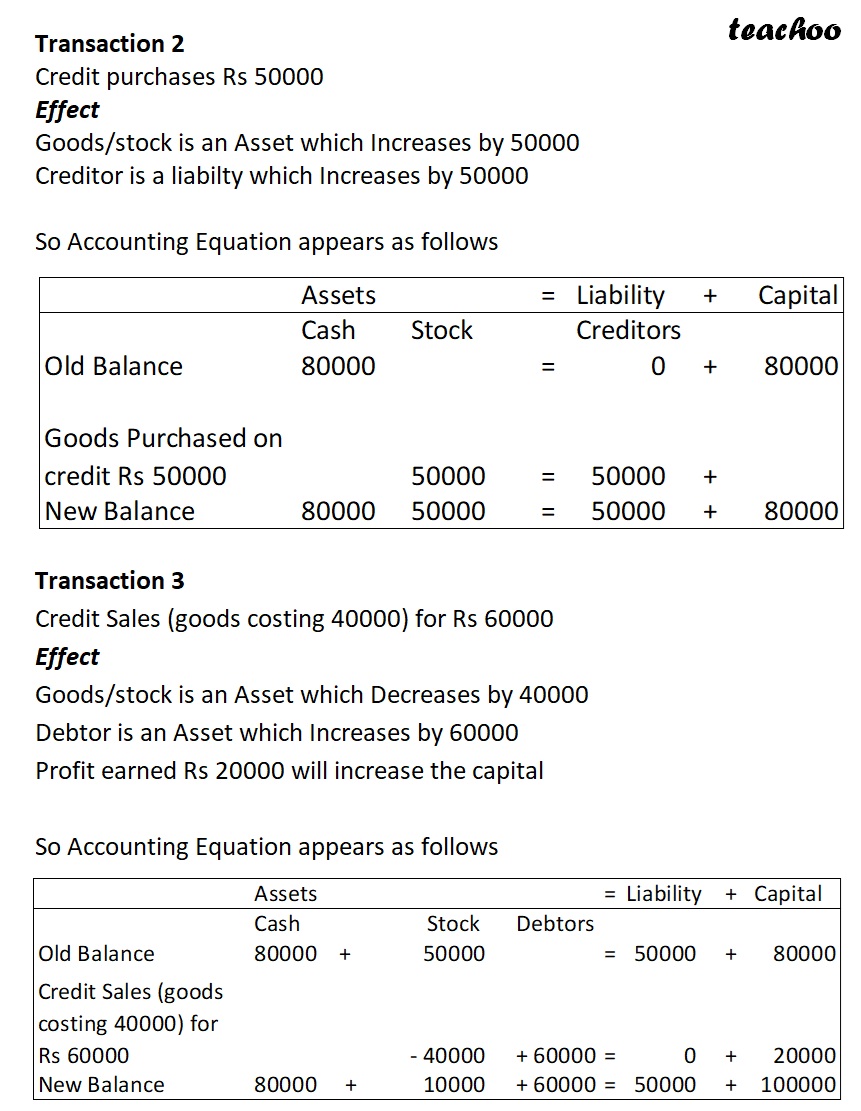

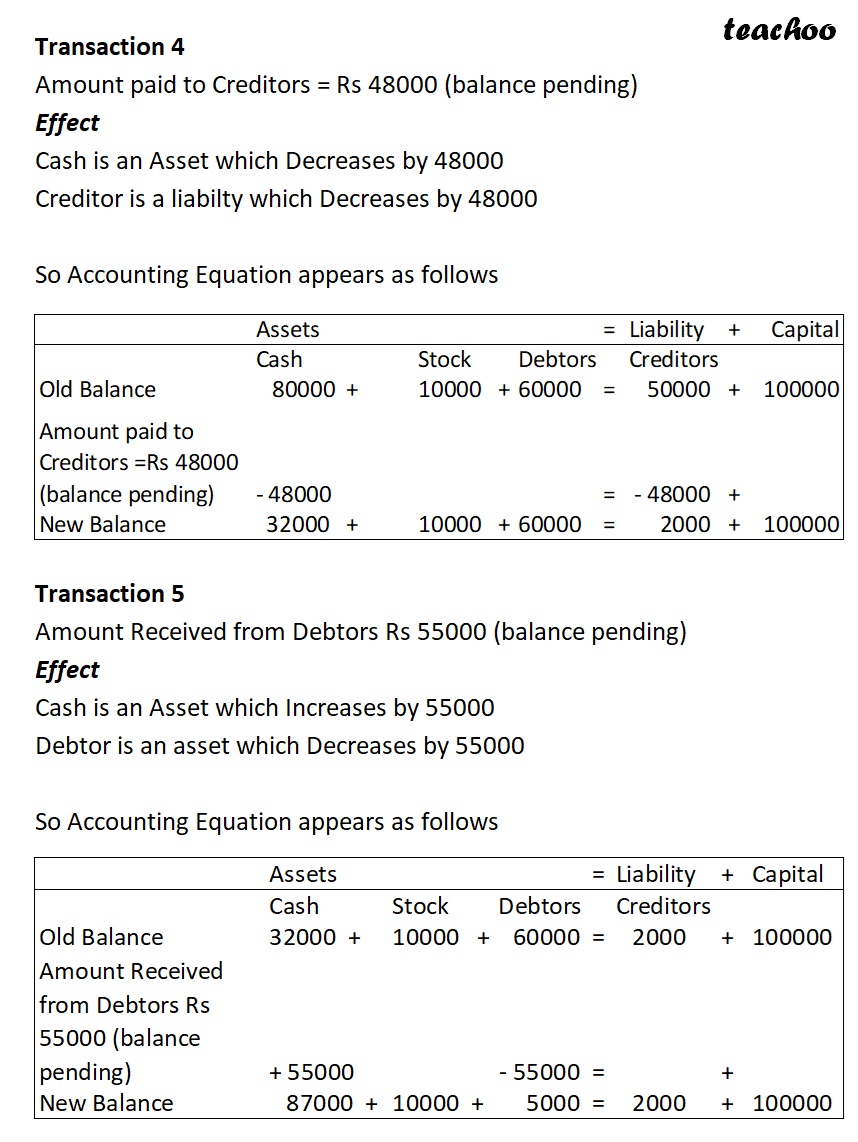

Transcript

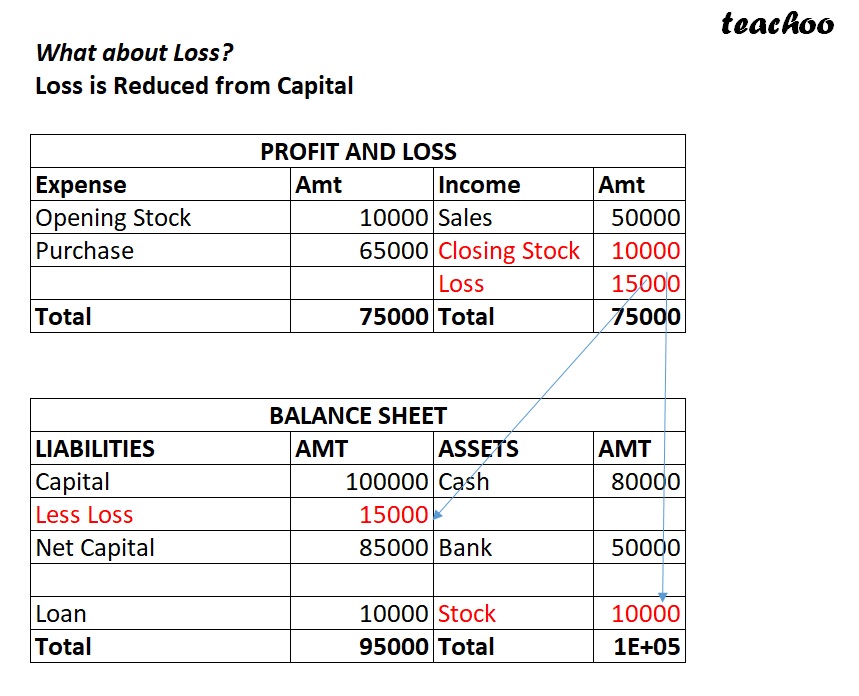

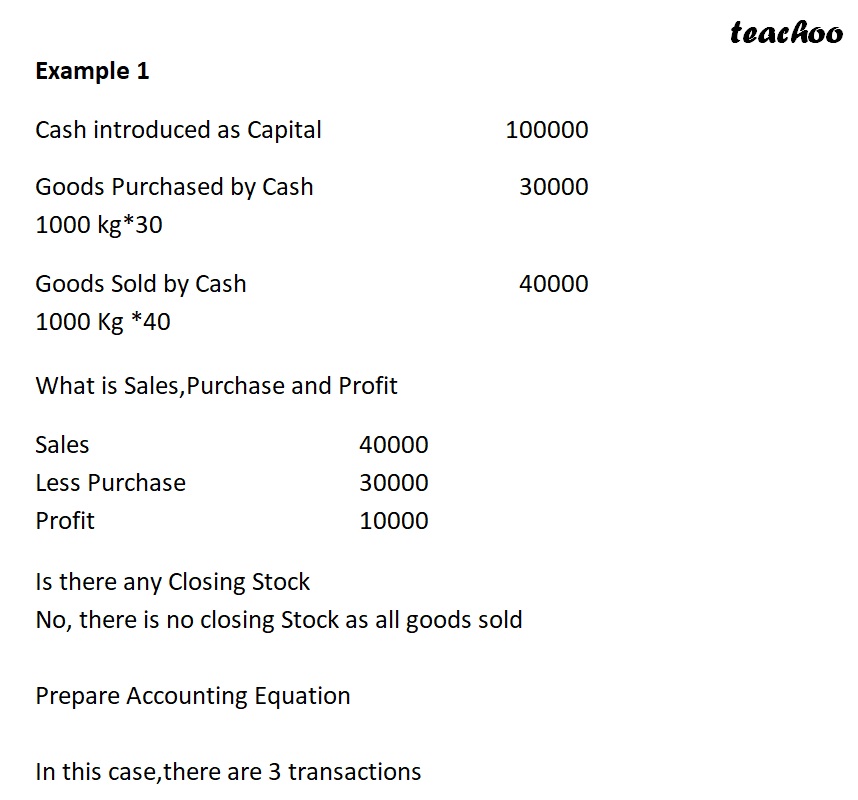

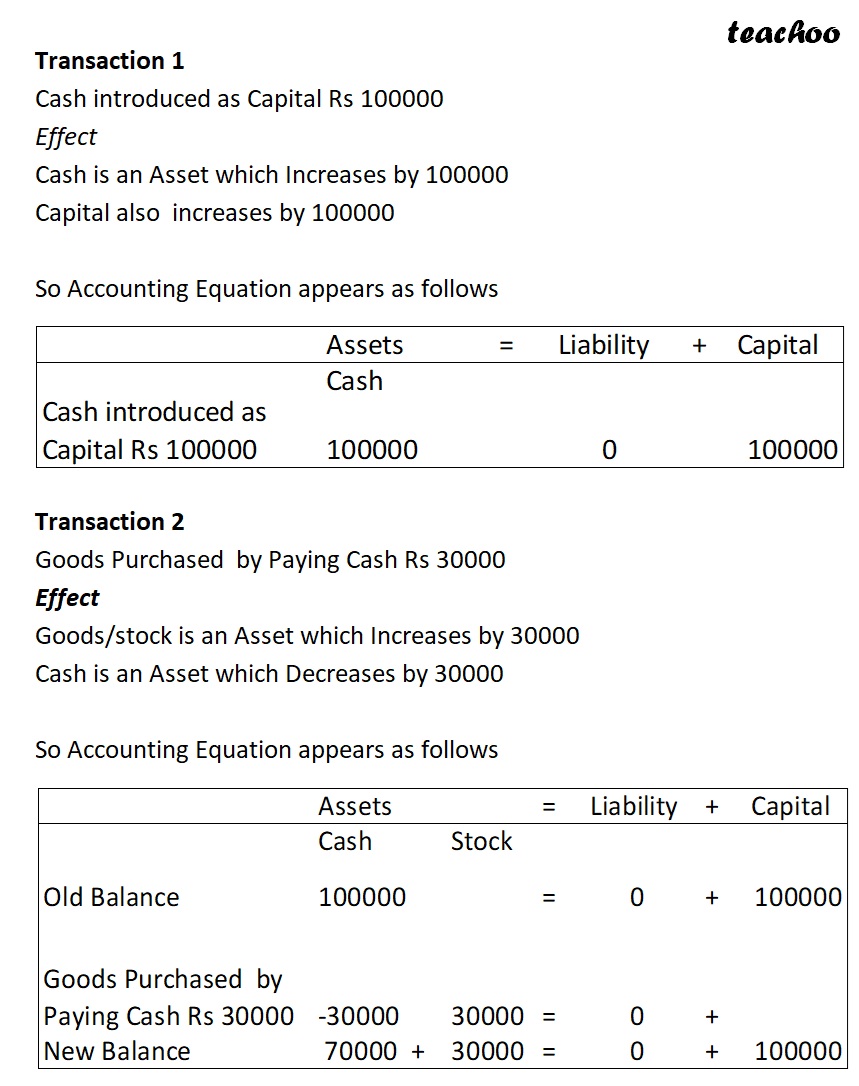

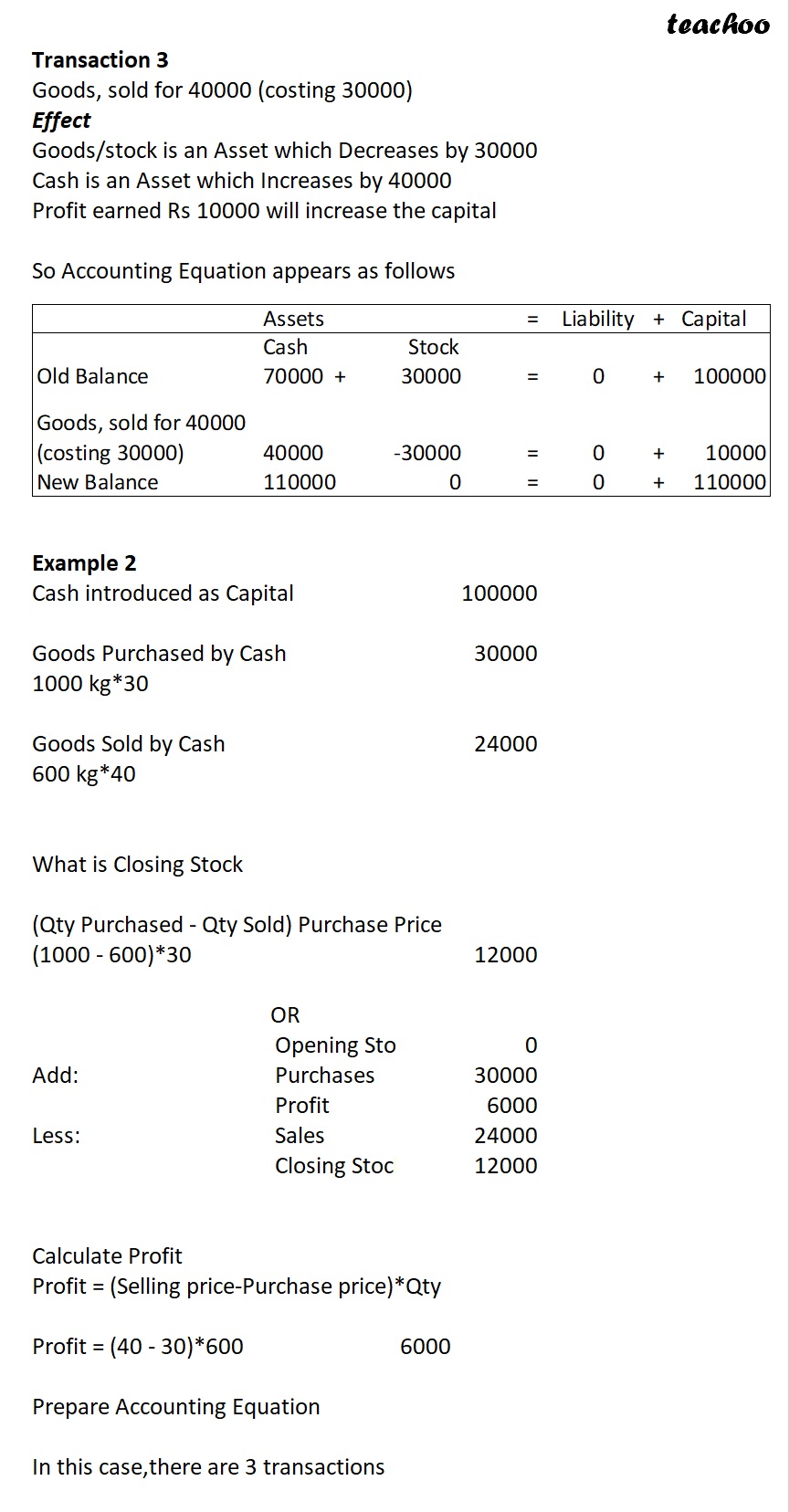

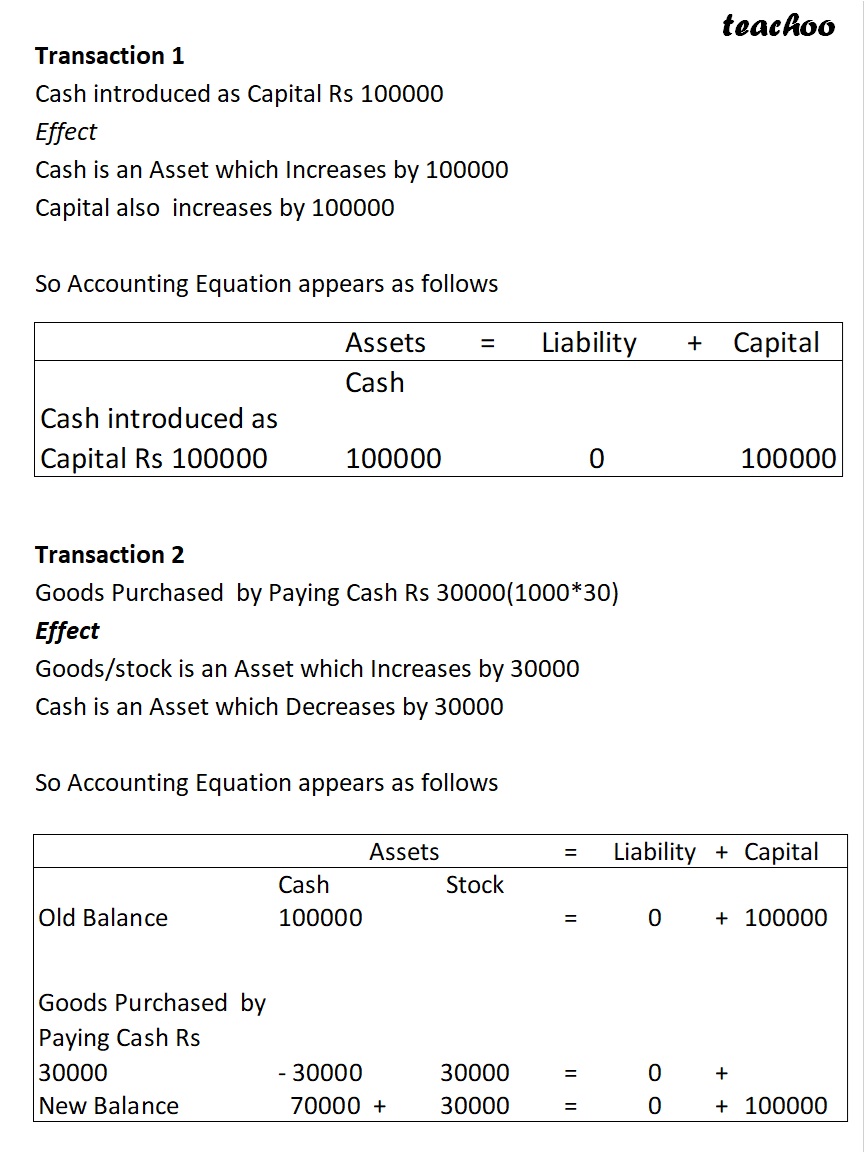

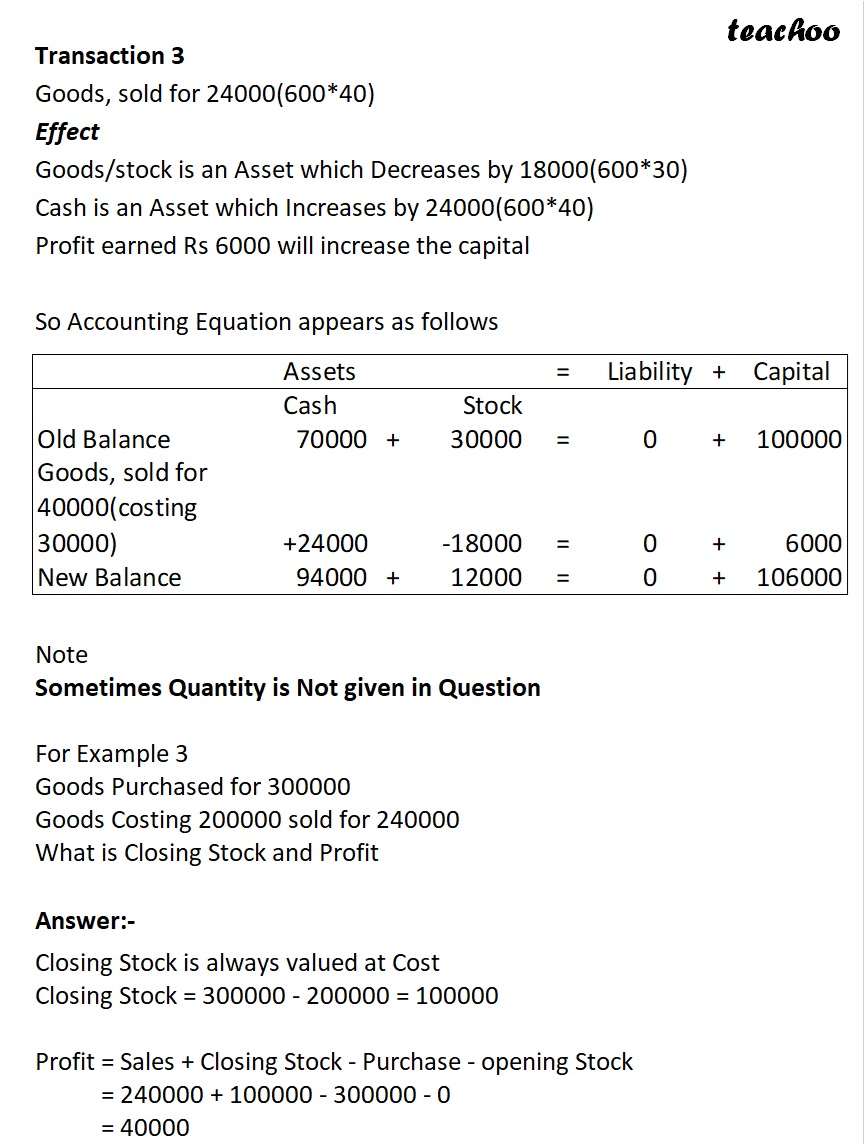

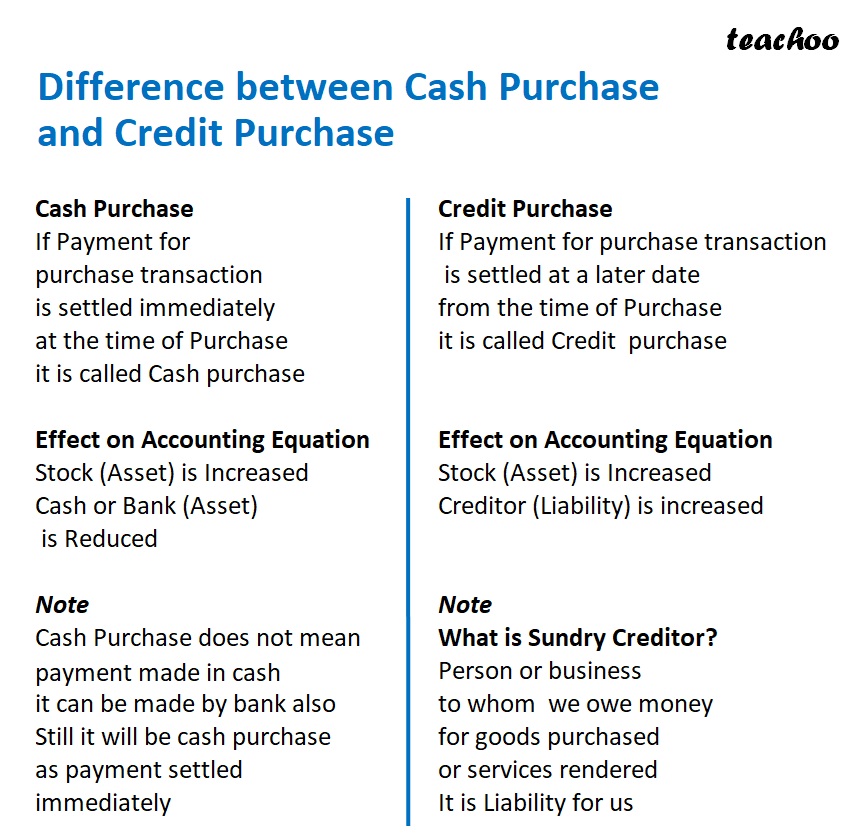

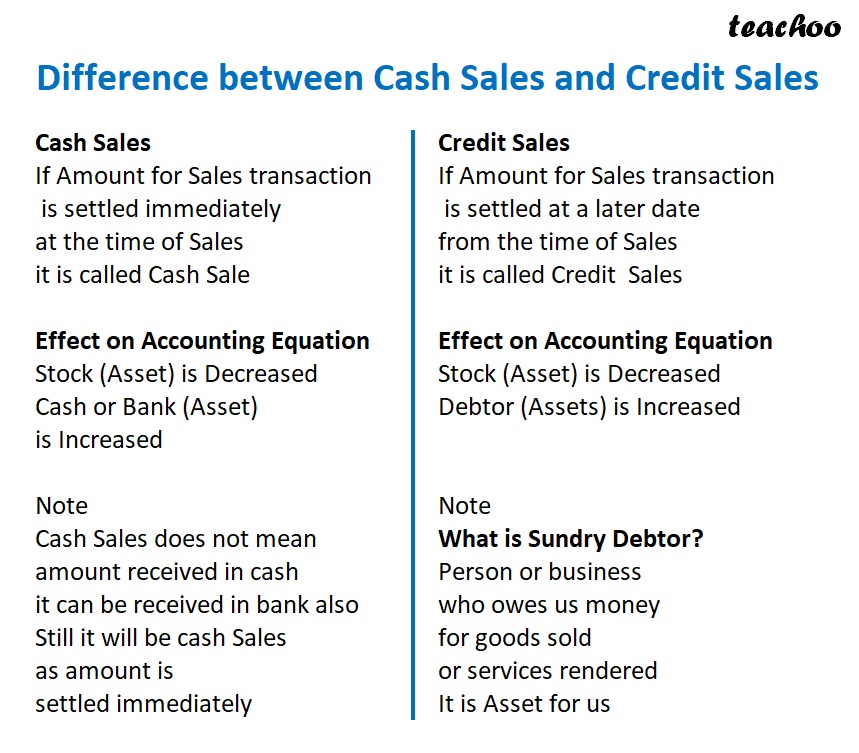

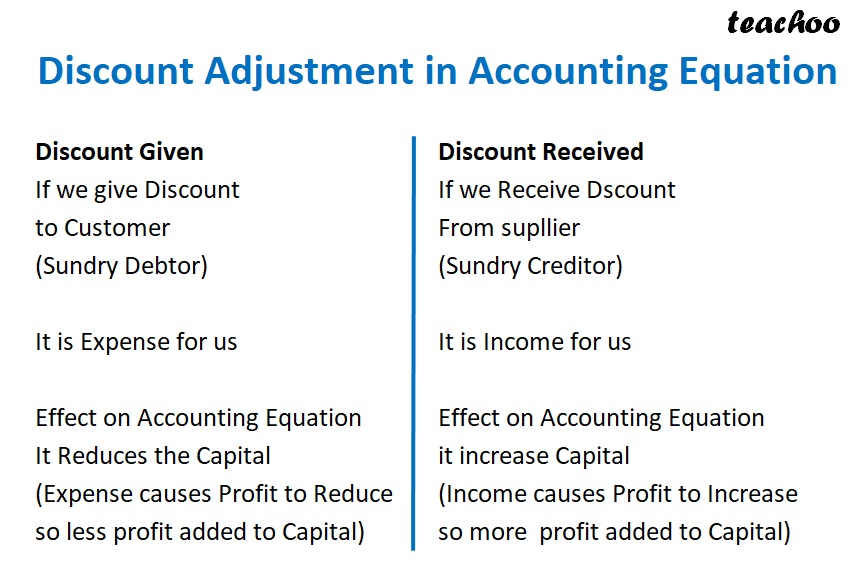

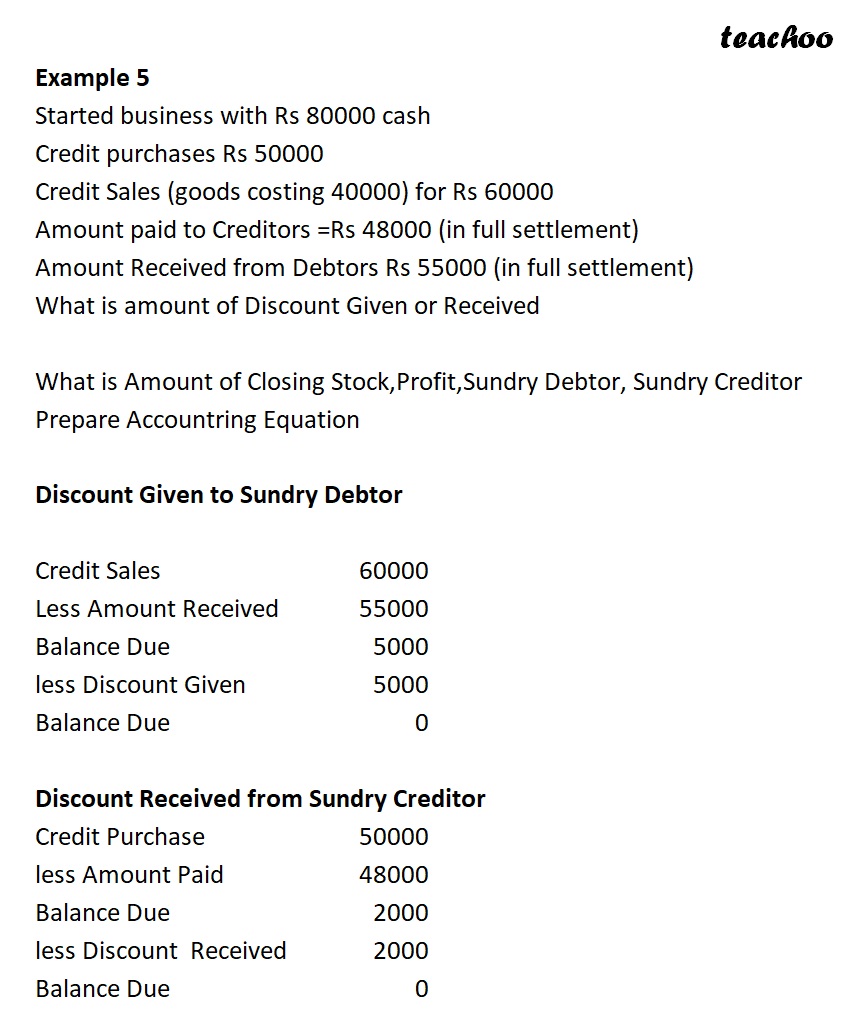

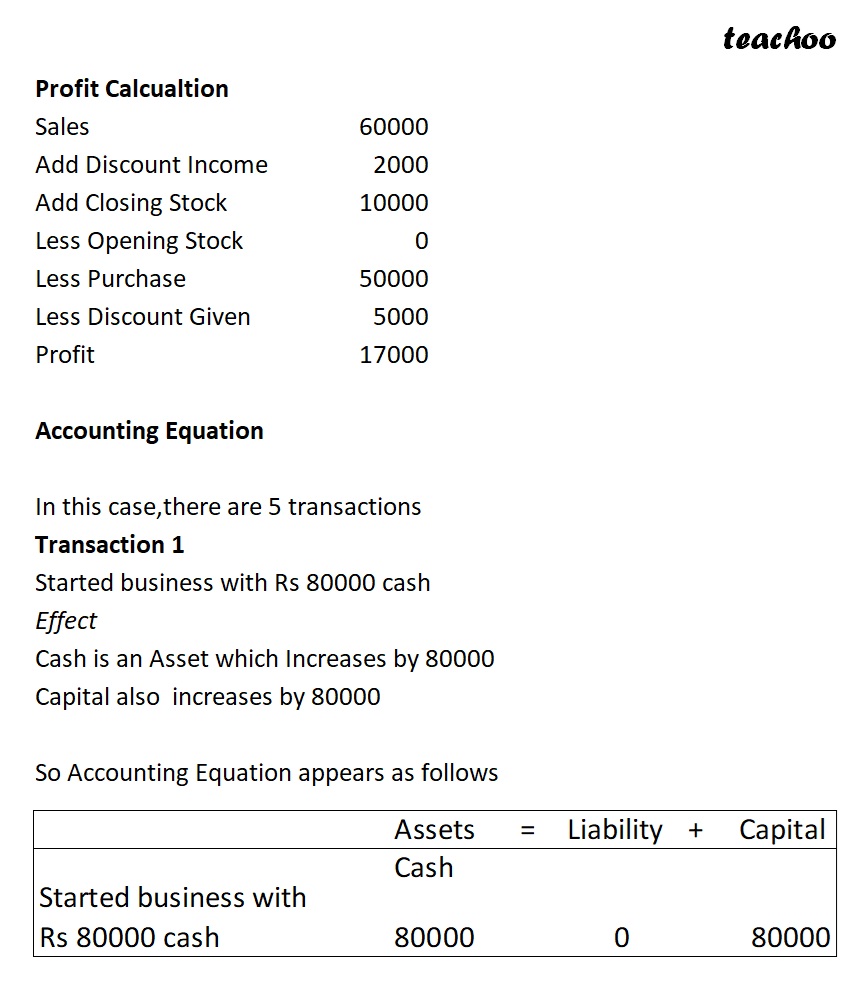

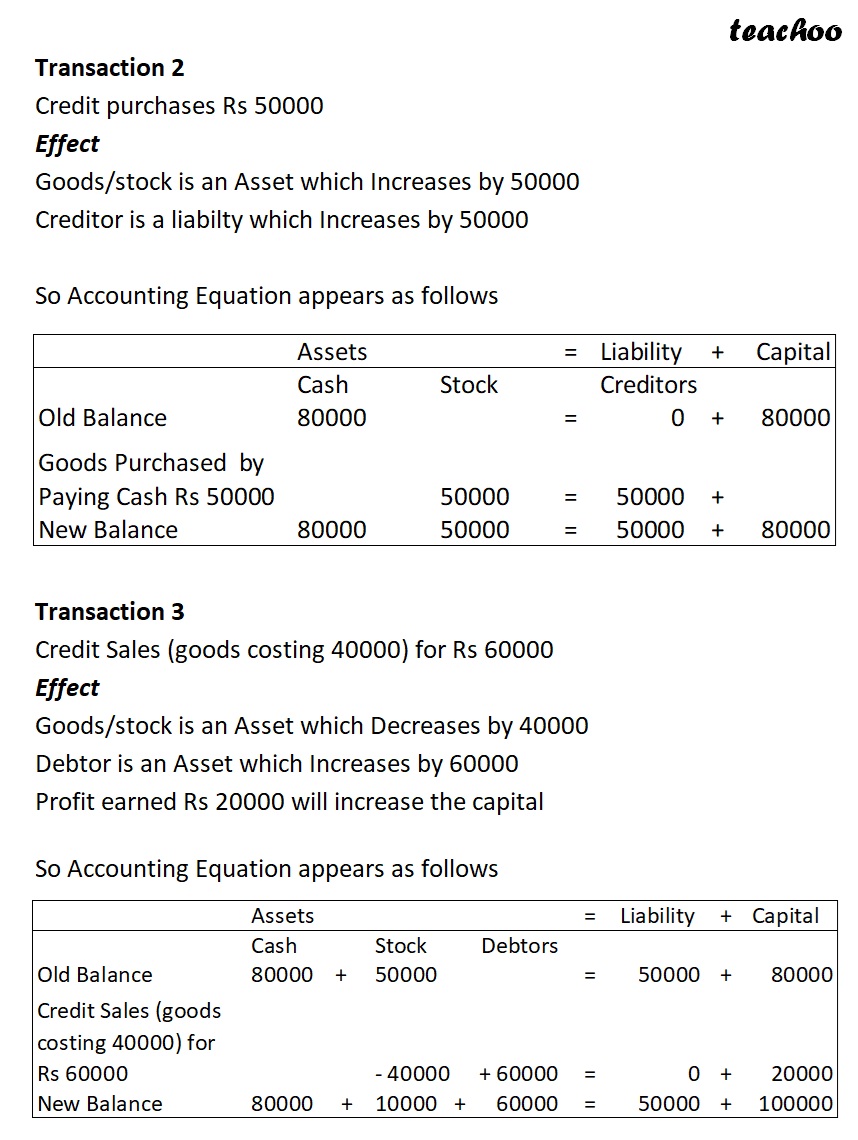

Accounting Equation for Purchase, Sales and Stock Common things in Profit and Loss and Balance sheet Only 2 things are Common Profit Closing Stock PROFIT AND LOSS Expense Amt Income Amt Opening Stock 10000 Sales 50000 Purchase 30000 Closing Stock 10000 Profit 20000 Total 60000 Total 60000 BALANCE SHEET LIABILITIES AMT ASSETS AMT Capital 100000 Cash 80000 Add Profit 20000 Total Capital 120000 Bank 50000 Loan 10000 Stock 10000 --> Closing Stock comes Total 130000 Total 130000 --> What about Loss? Loss is Reduced from Capital PROFIT AND LOSS Expense Amt Income Amt Opening Stock 10000 Sales 50000 Purchase 65000 Closing Stock 10000 Loss 15000 Total 75000 Total 75000 BALANCE SHEET LIABILITIES AMT ASSETS AMT Capital 100000 Cash 80000 Less Loss 15000 Net Capital 85000 Bank 50000 Loan 10000 Stock 10000 Total 95000 Total 130000 Example 1 Cash introduced as Capital 100000 Goods Purchased by Cash 30000 1000 kg*30 Goods Sold by Cash 40000 1000 Kg *40 What is Sales,Purchase and Profit Sales 40000 Less Purchase 30000 Profit 10000 Is there any Closing Stock No,there is no closing Stock as all goods sold Prepare Accounting Equation In this case,there are 3 transactions Transaction 1 Cash introduced as Capital Rs 100000 Effect Cash is an Asset which Increases by 100000 Capital also increases by 100000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Cash introduced as Capital Rs 100000 100000 0 100000 Transaction 2 Goods Purchased by Paying Cash Rs 30000 Effect Goods/stock is an Asset which Increases by 30000 Cash is an Asset which Decreases by 30000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Stock Old Balance 100000 = 0 + 100000 Goods Purchased by Paying Cash Rs 30000 -30000 30000 = 0 + New Balance 70000 + 30000 = 0 + 100000 Transaction 3 Goods ,sold for 40000(costing 30000) Effect Goods/stock is an Asset which Decreases by 30000 Cash is an Asset which Increases by 40000 Profit earned Rs 10000 will increase the capital So Accounting Equation appears as follows Assets = Liability + Capital Cash Stock Old Balance 70000 + 30000 = 0 + 100000 Goods ,sold for 40000(costing 30000) +40000 -30000 = 0 + 10000 New Balance 110000 0 = 0 + 110000 Example 2 Cash introduced as Capital 100000 Goods Purchased by Cash 30000 1000 kg*30 Goods Sold by Cash 24000 600 kg*40 What is Closing Stock (Qty Purchased- Qty Sold)purchase price (1000-600)30 12000 OR Opening Stock 0 Add: Purchases 30000 Profit 6000 Less: Sales 24000 Closing Stock 12000 Calculate Profit Profit = (Selling price-Purchase price)*Qty Profit = (40-30)*600 6000 Prepare Accounting Equation In this case,there are 3 transactions Transaction 1 Cash introduced as Capital Rs 100000 Effect Cash is an Asset which Increases by 100000 Capital also increases by 100000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Cash introduced as Capital Rs 100000 100000 0 100000 Transaction 2 Goods Purchased by Paying Cash Rs 30000(1000*30) Effect Goods/stock is an Asset which Increases by 30000 Cash is an Asset which Decreases by 30000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Stock Old Balance 100000 = 0 + 100000 Goods Purchased by Paying Cash Rs 30000 -30000 30000 = 0 + New Balance 70000 + 30000 = 0 + 100000 Transaction 3 Goods ,sold for 24000(600*40) Effect Goods/stock is an Asset which Decreases by 18000(600*30) Cash is an Asset which Increases by 24000(600*40) Profit earned Rs 6000 will increase the capital So Accounting Equation appears as follows Assets = Liability + Capital Cash Stock Old Balance 70000 + 30000 = 0 + 100000 Goods ,sold for 40000(costing 30000) +24000 -18000 = 0 + 6000 New Balance 94000 + 12000 = 0 + 106000 Note Sometimes Quantity is Not given in Question For Example 3 Goods Purchased for 300000 Goods Costing 200000 sold for 240000 What is Closing Stock and Profit Ans Closing Stock is always valued at Cost Closing Stock=300000-200000=100000 Profit=Sales+Closing Stock-Purchase-opening Stock =240000+100000-300000-0 =40000 Difference between Cash Purchase and Credit Purchase Cash Purchase Credit Purchase If Payment for If Payment for purchase transaction purchase transaction is settled at a later date is settled immediately from the time of Purchase at the time of Purchase it is called Credit purchase it is called Cash purchase Effect on Accounting Equation Effect on Accounting Equation Stock (Asset) is Increased Stock (Asset) is Increased Cash or Bank (Asset) Creditor (Liability) is increased is Reduced Note Note Cash Purchase does not mean What is Sundry Creditor? payment made in cash Person or business it can be made by bank also to whom we owe money Still it will be cash purchase for goods purchased as payment settled or services rendered immediately It is Liability for us Difference between Cash Sales and Credit Sales Cash Sales Credit Sales If Amount for Sales transaction If Amount for Sales transaction is settled immediately is settled at a later date at the time of Sales from the time of Sales it is called Cash Sale it is called Credit Sales Effect on Accounting Equation Effect on Accounting Equation Stock (Asset) is Decreased Stock (Asset) is Decreased Cash or Bank (Asset) Debtor (Assets) is Increased is Increased Note Note Cash Sales does not mean What is Sundry Debtor? amount received in cash Person or business it can be received in bank also who owes us money Still it will be cash Sales for goods sold as amount is or services rendered settled immediately It is Asset for us Example 4 Started business with Rs 80000 cash Credit purchases Rs 50000 Credit Sales (goods costing 40000) for Rs 60000 Amount paid to Creditors =Rs 48000 (balance pending) Amount Received from Debtors Rs 55000 (balance pending) What is Amount of Closing Stock,Profit,Sundry Debtor,Sundry Creditor Prepare Accountring Equation Closing Stock Closing Stock is always valued at Cost Closing Stock=50000-40000=10000 Profit=Sales+Closing Stock-Purchase-openng Stock =60000+10000-50000-0 =20000 Sundry Debtor Credit Sales 60000 Less Amount Received 55000 Balance Due 5000 Sundry Creditor Credit Purchase 50000 less Amount Paid 48000 Balance Due 2000 Accouting Equation In this case,there are 5 transactions Transaction 1 Started business with Rs 80000 cash Effect Cash is an Asset which Increases by 80000 Capital also increases by 80000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Started business with Rs 80000 cash 80000 0 80000 Transaction 2 Credit purchases Rs 50000 Effect Goods/stock is an Asset which Increases by 50000 Creditor is a liabilty which Increases by 50000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Stock Creditors Old Balance 80000 = 0 + 80000 Goods Purchased on credit Rs 50000 50000 = 50000 + New Balance 80000 50000 = 50000 + 80000 Transaction 3 Credit Sales (goods costing 40000) for Rs 60000 Effect Goods/stock is an Asset which Decreases by 40000 Debtor is an Asset which Increases by 60000 Profit earned Rs 20000 will increase the capital So Accounting Equation appears as follows Assets = Liability + Capital Cash Stock Debtors Old Balance 80000 + 50000 = 50000 + 80000 Credit Sales (goods costing 40000) for Rs 60000 -40000 +60000 = 0 + 20000 New Balance 80000 + 10000 + 60000 = 50000 + 100000 Transaction 4 Amount paid to Creditors =Rs 48000 (balance pending) Effect Cash is an Asset which Decreases by 48000 Creditor is a liabilty which Decreases by 48000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Stock Debtors Creditors Old Balance 80000 + 10000 + 60000 = 50000 + 100000 Amount paid to Creditors =Rs 48000 (balance pending) -48000 = -48000 + New Balance 32000 + 10000 + 60000 = 2000 + 100000 Transaction 5 Amount Received from Debtors Rs 55000 (balance pending) Effect Cash is an Asset which Increases by 55000 Debtor is an asset which Decreases by 55000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Stock Debtors Creditors Old Balance 32000 + 10000 + 60000 = 2000 + 100000 Amount Received from Debtors Rs 55000 (balance pending) +55000 -55000 = + New Balance 87000 + 10000 + 5000 = 2000 + 100000 Discount Adjustment in Accounting Equation Discount Given Discount Received If we give Discount If we Receive Dscount to Customer From supllier (Sundry Debtor) (Sundry Creditor) It is Expense for us It is Income for us Effect on Accounting Equation Effect on Accounting Equation It Reduces the Capital it increase Capital (Expense causes Profit to Reduce (Income causes Profit to Increase so less profit added to Capital) so more profit added to Capital) Example 5 Started business with Rs 80000 cash Credit purchases Rs 50000 Credit Sales (goods costing 40000) for Rs 60000 Amount paid to Creditors =Rs 48000 (in full settlement) Amount Received from Debtors Rs 55000 (in full settlement) What is amount of Discount Given or Received What is Amount of Closing Stock,Profit,Sundry Debtor,Sundry Creditor Prepare Accountring Equation Discount Given to Sundry Debtor Credit Sales 60000 Less Amount Received 55000 Balance Due 5000 less Discount Given 5000 Balance Due 0 Discount Received from Sundry Creditor Credit Purchase 50000 less Amount Paid 48000 Balance Due 2000 less Discount Received 2000 Balance Due 0 Profit Calcualtion Sales 60000 Add Discount Income 2000 Add Closing Stock 10000 Less Opening Stock 0 Less Purchase 50000 Less Discount Given 5000 Profit 17000 Accounting Equation In this case,there are 5 transactions Transaction 1 Started business with Rs 80000 cash Effect Cash is an Asset which Increases by 80000 Capital also increases by 80000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Started business with Rs 80000 cash 80000 0 80000 Transaction 2 Credit purchases Rs 50000 Effect Goods/stock is an Asset which Increases by 50000 Creditor is a liabilty which Increases by 50000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Stock Creditors Old Balance 80000 = 0 + 80000 Goods Purchased by Paying Cash Rs 50000 50000 = 50000 + New Balance 80000 50000 = 50000 + 80000 Transaction 3 Credit Sales (goods costing 40000) for Rs 60000 Effect Goods/stock is an Asset which Decreases by 40000 Debtor is an Asset which Increases by 60000 Profit earned Rs 20000 will increase the capital So Accounting Equation appears as follows Assets = Liability + Capital Cash Stock Debtors Old Balance 80000 + 50000 = 50000 + 80000 Credit Sales (goods costing 40000) for Rs 60000 -40000 +60000 = 0 + 20000 New Balance 80000 + 10000 + 60000 = 50000 + 100000 Transaction 4 Amount paid to Creditors =Rs 48000 (in full settlement) Effect Cash is an Asset which Decreases by 48000 Creditor is a liabilty which Decreases by 50000 Discount Received will increase the capital by 2000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Stock Debtors Creditors Old Balance 80000 + 10000 + 60000 = 50000 + 100000 Amount paid to Creditors =Rs 48000 (balance pending) -48000 = -50000 + 2000 New Balance 32000 + 10000 + 60000 = 0 + 102000 Transaction 5 Amount Received from Debtors Rs 55000 (in full settlement) Effect Cash is an Asset which Increases by 55000 Debtor is an asset which Decreases by 60000 Discount allowed will reduce the capital by 5000 So Accounting Equation appears as follows Assets = Liability + Capital Cash Stock Debtors Creditors Old Balance 32000 + 10000 + 60000 = 2000 + 100000 Amount Received from Debtors Rs 55000 (balance pending) +55000 -60000 = + -5000 New Balance 87000 + 10000 + 0 = 2000 + 95000