![What is Opening and Closing Stock? [Class 11 Accountancy] - Teachoo - Chapter 1 - Introduction to Accounting](https://cdn.teachoo.com/1ffe2077-6ccf-4b52-8030-b39ea4bd5ea7/slide-1-what-is-stock-inventory.jpg)

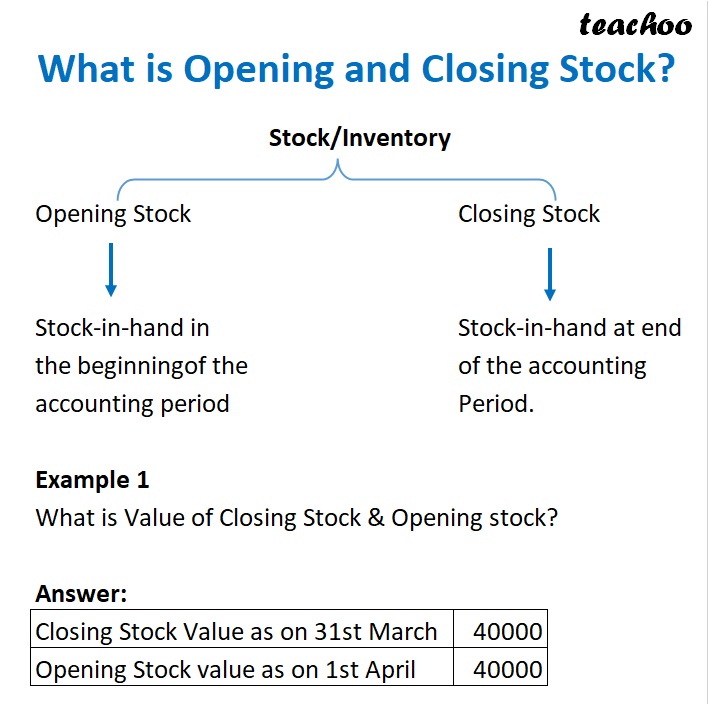

Question 1

Select the correct alternative:

Stock is valued at

(a) Cost or Net Realisable Value (Market Value), whichever is less.

(b) Cost or Net Realisable Value (Market Value), whichever is more.

(c) Cost.

(d) Net Realisable Value (Market Value).

Answer:

(a) Cost or Net Realisable Value (Market Value), whichever is less

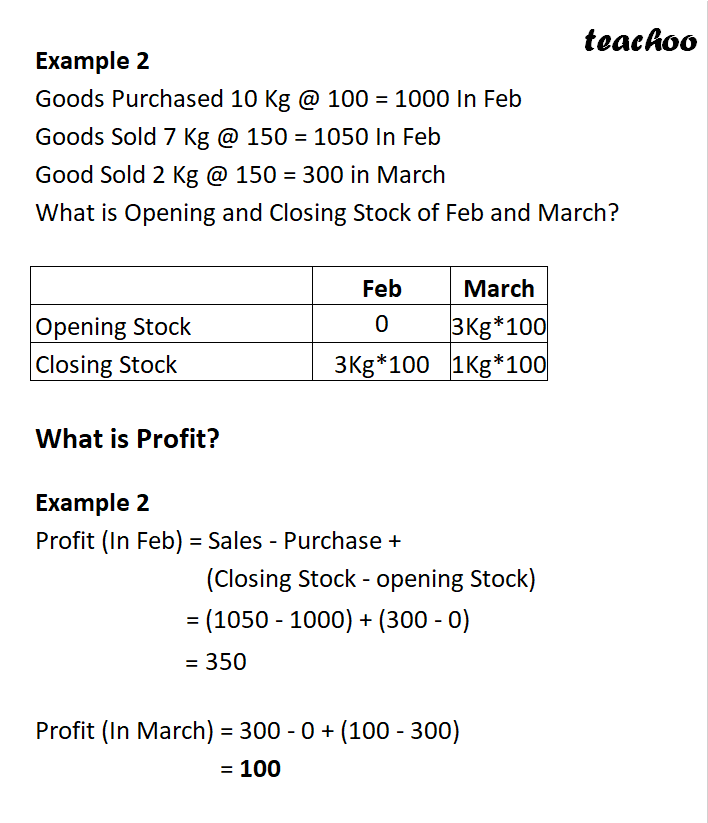

Question 12

Assertion (A): Goods remaining unsold at the end of the accounting year are termed ‘Stock’.

Reason (R): Stock includes fixed assets remaining unused at the end of the accounting year.

On the basis of the following two statements, identify the correct option out of the following:-

(a) Both Assertion (A) and Reason (R) are correct but Reason (R) is not the correct explanation of the Assertion (A)

(b) Both Assertion (A) and Reason (R) are correct and Reason (R) is the correct explanation of the Assertion (A)

(c) Both Assertion (A) and Reason (R) are not correct

(d) Assertion (A) is correct but Reason (R) is not correct

Answer:

(d) Assertion (A) is correct but Reason (R) is not correct

Competency Based Questions

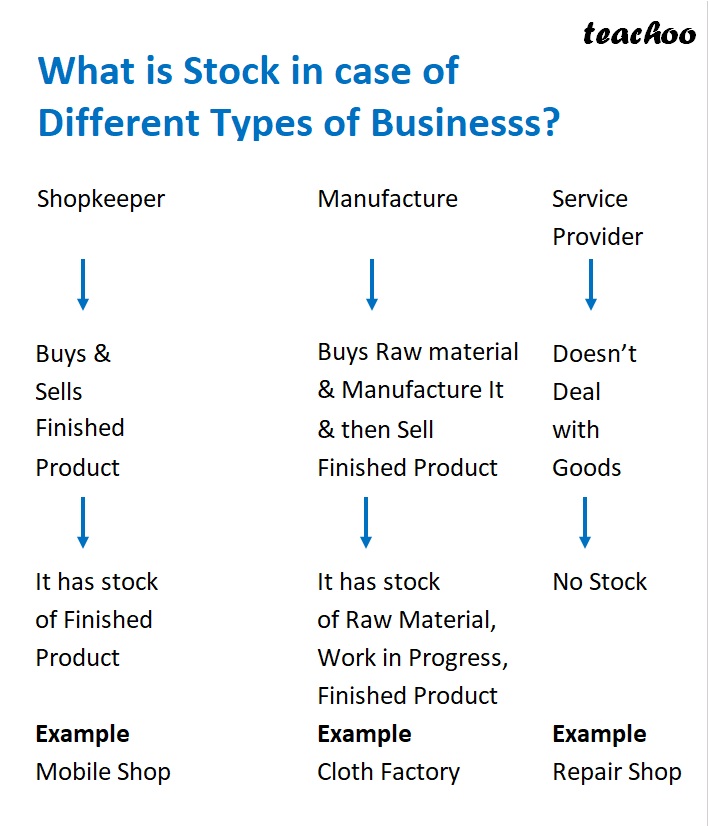

Question 3

A manufacturing firm classifies its Inventory (Stock) in

(a) Raw Materials.

(b) Work-in-Progress.

(c) Finished Goods.

(d) All of these.

Answer:

(d) All of these.

Question 6

A firm purchased goods of ₹ 10,00,000 during the financial year ended 31st March, 2025. As on 31st March, 2025, unsold stock is of ₹ 50,000. Is this an event and why?

Answer:

Closing Stock of ₹ 50,000 on 31st March, 2025 is an event resulting out of purchase of goods of ₹ 10,00,000 during the year ended 31st March, 2025.