E-Way Bill Validity Changed from 1 Jan 2021

Earlier, E-Way Bill Validity was 1 day for Every 100 Km or part thereof

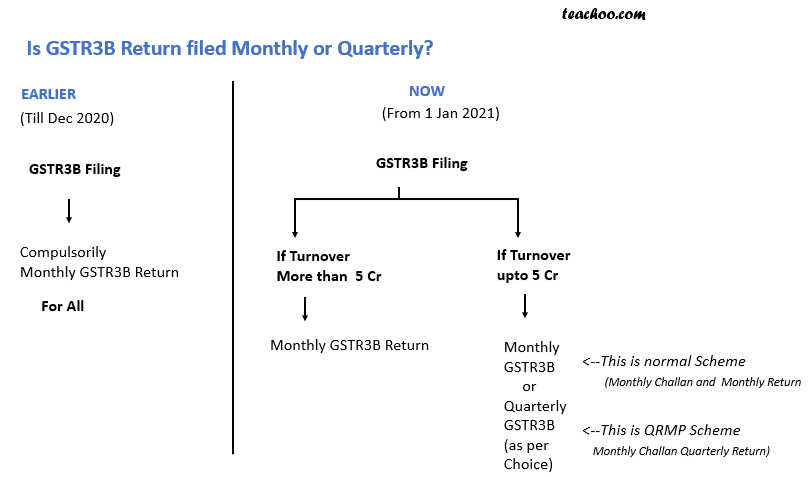

QRMP Scheme from 1 Jan 2021

What are GSTR3B Return Due Dates for QRMP Scheme

What is Challan Due Date in QRMP Scheme

GSTR1 Due Date Changed for Quarterly Tax Payers

Concept of Invoice Furnishing Facility for Quarterly GSTR1

Due Dates for GSTR1 and IFF

Compulsory 1% Cash payment if Turnover More than 50 lacs

GSTR3B Return Form Autopopulated

Provisional Credit Restricted to 5% from Jan 2021

NEW AMENDMENT IN GSTR1 IF TURNOVER IS UPTO 1.5 CRORES-FROM 1 OCT 2020

Earlier- If Turnover upto 1.5 crore,GST1 could be Quarterly or Monthly

Quarterly-One month from end of Quarter

Monthly-11th of Next Month

Now- If Turnover upto 1.5 crore,GST1 could be Quarterly only

Quarterly-13 Days from end of quarter

Monthly- Can't file monthly if turnover upto 1.5 crore

Changes in the Annual Return(GSTR9) Due Dates

2018-19- Due date has been extended from 31st Dec 2019 to 31st Dec 2020

2019-20- Original date is 31st Dec 2019,which hasn't been extended as of now

GSTR9 and GST9C Changes

As per Original Rule-

GSTR9(Annual Return)-Compulsory for all

GSTR9C -If turnover is more than 2 Crore

As per Amendment-

GSTR9(Annual Return)-Optional if turnover upto 2 crore

GSTR9C-If turnover is more than 5 crore

Changes in HSN Code Requirement of Tax Invoice

HSN Code required on Tax Invoice has increased from 1st April 2021 as follows-

If turnover in Previous Year is upto 5 crore HSN Code is 4 Digit(B2B Only)

If turnover is more than 5 crore HSN code is 6 digit

If turnover upto 5 crore, than HSN number is not required if sales to unregistered

Return Filed by EVC or DSC

Return can be filed by EVC( Everification Code or OTP) only in case of Non-Companies

or

DSC (Digital Signature) Can be filed by all

EVC can also be used by companies till 31st Oct 2020

GSTR4 Due Date Extended for FY 2019-20

GST4 original due date was 30 April of Next Year

Hence Due Date for FY 2019-20 was 30 April 2020

It has been last extended to 31 Oct 2020 due to Lockdown

Other Amendments

Changes In GST (37th GST Council meeting held in Goa)

Annual return GSTR 9 is to be made optional, if turnover upto 2 Crore for F.Y. 2017-18 & 2018-19.

However, if turnover more than 2 crore then both GSTR 9 and GSTR 9C is to be filed

New Return Forms

The existing return forms GSTR 3B and GSTR 1 will be replaced by three new return forms

- GST Normal Return (Monthly/Quaterly)

- GST Sahaj Return

- GST Sugam Return

Whether Returns to be Filed Monthly or Quarterly

Those having turnover more than 5 Crores have to file Normal(Monthly) Returns

However, those having turnover upto 5 crores can chose Normal (Monthly /Quarterly)Returns

Note: - Last year turnover is to be taken .However for new business, likely turnover of current year is to be taken to determine whether turnover is monthly or quarterly

Trial run of new return forms

Trial run of offline tool of new return of GST is available at GST website.

Changes In Composition Scheme Return Filing

Composition dealer needs to pay tax quarterly by 18th of next quarter in form CMP-08 and file return annually GSTR 4

| PERIOD | DUE DATE | RETURN/PAYMENT FORM NAME |

| APRIL-JUNE | 18/07/2018 31/08/2019 | CMP-08(PAYMENT FORM) |

| JULY-SEPTEMBER | 18-Oct-18 | CMP-08(PAYMENT FORM) |

| OCTOBER-DECEMBER | 18-Jan-19 | CMP-08(PAYMENT FORM) |

| JANUARY-MARCH | 18-Apr-19 | CMP-08(PAYMENT FORM) |

| APRIL 2019-MARCH 2020 | 30-Apr-20 | GSTR -4 (RETURN) |

Due date for filing intimation in FORM CMP-02 extended to 30.09.2019

Last date for filing intimation , in FORM GST CMP-02 , to avail benefit of Notification no. 2/2019 dated 07.03.2019 has been extended to 30.09.2019

GSTR 3B Filing Extended

GSTR3B was to be filed only from July 2017 to Dec 2017, Now,it has been extended to September 2019 for quaterly scheme and November 2019 for monthly scheme

Annual Return Due Date Extended

Due date for

GSTR 9,GSTR 9A,GSTR 9C for FY 2017-18 extended to 31st December 2019

Due Date For Gstr 7(Tds Return) Extended

Due date for TDS Return from October 2018 to June 2019 is extended to 31st August 2019

Registration Limit Increased For Goods

Registration Limit

FOR GOODS

If Aggregate Turnover is greater than 40 lacs or likely to exceed 40 lacs, then Compulsory Registration is required (Amendment from 01.04.2019)

(Limit is 20 lacs for North Eastern States) (Amendment from 01.02.2019)

FOR SERVICES

If Aggregate Turnover is greater than 20 lacs or likely to exceed 20 lacs, then Compulsory Registration

(Limit is 10 lacs for North Eastern States)

Compositions scheme now available to all service providers

New Amendment from 1 April 2019

- In case of service provider (except restaurant)

- If turnover is upto 50 lac, then 6% Rate of tax for composition scheme

- Till 31st March 2019, composition scheme was not available to such service provider

|

Type of Business |

TILL 31 DEC 2017 |

FROM 1 JAN 2018 |

FROM 1 APRIL 2019 |

|

Trader |

1% |

1% |

1% |

|

Manufacturer |

2% |

2% 1% |

2% 1% |

|

Restaurant |

5% |

5% |

5% |

|

Other services |

N/A |

N/A | 6% |

Turnover Limit for composition scheme changed

If turnover upto 100 lacs, then Composition Scheme can be availed

This to be shown in increase to 150 lacs from 1st April 2019

For north eastern state and Uttarakhand limit has been increased from 50 lac to 75 lac

GSTR 9 (Annual return) now available at GST website

Online filing of GSTR 9 has been made active on the GST portal. It can be accessed after logging in the portal and selecting Services -> Returns -> Annual Return.

Important points

1. There is no facility for revision of GSTR 9. Therefore, it is advised to file GSTR 9 with utmost care.

2. Online filing tool is available in cases where the number of records in Table 17 (HSN wise summary of outward supplies) or Table 18 (HSN wise summary of inward supplies) are upto 500.

3. Where number of records exceed 500 in Table 17 or 18, then filing will be facilitated through offline utility only. Offline utility is not available for download as of now, but it is expected to be activated very soon.

4. A summary of GSTR 9 is available on the portal for downloading which is based on the GSTR 1 and 3B already filed by the registered person. Such summary is only for representational purpose and the facility to make changes in the fields reflected in the GSTR 9 is available through the online filing tool.

5. Summarized GSTR 1 and 3B for FY 17-18 are also available for downloading.

6. After filling up the details in the respective tables, the registered taxpayer shall click on "Compute liability" button to ascertain the amount of liability. If there is any short payment, then payment of tax can be made through GST DRC-03. Such liability can be paid only in cash.

Due date due dates for annual returns 30th June 2019. Due date for GST audit and filing of reconciliation in GSTR 9C is also 30th June 2019,

GSTR 3B Due Date For Jan 2019 Extended

Due date was 20th Feb 2019, now it has been extended to 22nd Feb 2019

However for Jammu and Kashmir, it is 28 Feb 2019

Important changes in GST Adjustment Rules

From 1 Feb Government has made changes in how IGST Credit will be adjusted

Changes in GST Act from 31 st Jan

-

In case of inward supply from unregistered suppliers RCM shall be applicable to the notified persons and notified supply of goods/ services. −9(4)

Currently there is no notification in this regard (so this RCM is still not applicable) - Higher limit of turnover for composition scheme raised from Rs 1 Cr to Rs 1.5 Cr. – Section 10

- Composition dealers in goods allowed to supply services for a value not exceeding – Higher of 10% turnover or Rs 5 lacs, whichever is higher.

-

Taxpayers may opt for multiple registrations within a state/UT for different place of business having same PAN.

(Earlier it was possible only if we had different business vertical (diff business) - Registration shall remain temporary suspended till completion of cancellation (No return to be filled).

-

Threshold limit of turnover for exemption for special category states – Assam, Arunachal Pradesh, Himachal Pradesh, Meghalaya, Sikkim, Uttarakhand increased to Rs 20, 00,000.

-

Registered person may issue consolidated credit or debit notes to a party in respect of multiple invoices issued in a financial year to that party.

(earlier separate debit note credit note for diff invoices) - Change in blocked credit U/s 17(5)

- Change in definition of supply as specified in schedule III (Exclusion from Supply)

-

Mandatory registration is required only for those E- Commerce operator who is required to collect TCS

(earlier for all E-Commerce operators, registration was compulsory)

NICAI Updates:

Key updates of 31st GST Council Meeting.

- GST Rates of 7 items reduced from 28% to 18% . Items include tyres, VCR, billiards & snookers and lithium batteries.

- GST Rate of 33 items have come down from 18% tax slab to 12% and 5% tax bracket as they are common man’s consumption goods. These items include Third Party insurance Vehicle and Solar Power Systems

- Only 34 items will be taxed at 18% GST Rate or more

-

All items except luxury goods would be taxed under 28% GST Rate

- The GST Council is also looking into introducing composition scheme for the real estate sector. A view on Real Estate sector will be taken in next GST Council meeting

- A composition Scheme will be framed for Small Service provider. Threshold and mechanism will be decided in next GST Council Meeting

- MSME Committee may re-consider the thresh hold limit of 20 Lakh for larger interest.

- Centralized authority for Advance ruling in case of conflicting views of Advance Ruling Authorities. The decision of Centralized authority will bind the whole country.

- New GST Refund filing system will be introduced on pilot basis with effect from 1st April 2018

- Addition GST fees waived for returns filed upto 31st March 2019

- GST Annual return due date has been extended to 30th June 2019

- ITC for last FY invoices allowed upto March 31, 2019

- New GST Return to be launched on trial basis from April 1, 2019 Next GST Council meeting will be held in January 2019

- Late fee shall be completely waived for all taxpayers in case FORM GSTR-1, FORM GSTR-3B &FORM GSTR-4 for the months / quarters July, 2017 to September, 2018, are furnished after 22.12.2018 but on or before 31.03.2019.

- Due date for claiming ITC of FY 2017 18 Extended till March 2019

- Due date of furnishing GSTR8 for Oct to Dec 18 extended to 31.01.2019

- GST on Export of Services in case of Outsourcing of services

- Due date of FORM ITC 04 for the period July’17 to Dec’18 extended till 31.03.2019

UNIQUE COMMON ENROLLMENT FOR TRANSPORTER

A Transported registered in more than one state with same PAN No may apply for

Unique Common Enrollment No by submitting FORM ENR-02, provided he may not be able

to use old Good and Services Identification No.

Due Date for Gstr-6

Due Date for Gstr-6 From July 2017 to June 2018 has been Extended till 31st July 2018

LATE FOR GSTR-3B WAIVED IN SOME CASES

due date for each of the months from October,

2017 to April, 2018, for the class of registered persons whose declaration in FORM GST

TRAN-1 was submitted but not filed on the common portal on or before the 27th day of

December, 2017:

Provided that such registered persons have filed the declaration in FORM GST

TRAN-1 on or before the 10th day of May, 2018 and the return in FORM GSTR-3B for each

of such months, on or before the 31st day of May, 2018.

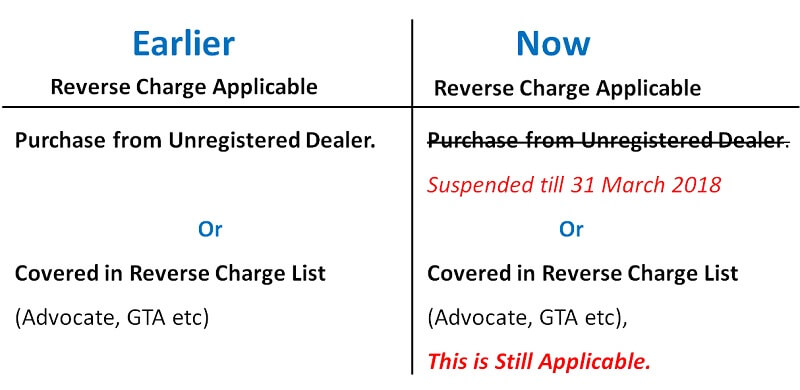

NO REVERSE CHARGE ON UNREGISTERED DEALER TILL 30 SEPTEMBER

Earlier reverse charge on unregistered dealer was suspended till 31st March now extended till 30th September

Learn more

E-WAY BILL FOR DELHI

E-way Bill are compulsory for intra state movement of in all states

However for delhi E Way bill is compulsory if amount is more than 100000(and not 50000)

Also it is compulsory only in case of B2B (and not B2C)

Note-For interstate sales,rules are same all over India

Different rules are only for intrastate in Delhi

GST Rate for Manufacturers also 1% in Composition Scheme

Government has changed GST Rates for Manufacturers from 2% to 1% vide Notification 1/2018

Hence, now GST Rates are similar for Traders and Manufacturers

Summary of Rates

|

Type of Business |

TILL 31 DEC 2017 |

FROM 1 JAN 2018 |

|

Trader |

1% |

1% |

|

Manufacturer |

2% |

2% 1% |

|

Restaurant |

5% |

% |

E-Way Bill Compulsory from 1 Feb 2018

E-Way Bill needs to be generated for movement of goods 50000 or more

Transporter has to carry this E way bil while moving goods from one placed to another

This has to be generated either

Online at E Way bill website ewaybill.nic.in

Or

Through SMS

This has been started in a trial manner from 16 Jan 2018 and will be compulsory from 1 Feb 2018

It will be mandatory from 1 April 2018

For details procedure refer

Due Dates of GST Returns Extended

1. Due dates for GSTR-1 for monthly tax payer

July - November, 2017

10th January, 2018

December, 2017

10th February, 2018

January, 2018

10th March, 2018

April, 2018

31st May, 2018

May, 2018

10th June, 2018

June, 2018

10th July, 2018

2. Due dates for GSTR-1 for quarterly tax payer

July - September, 2017

10th January, 2018

October - December, 2017

15th February, 2018

January - March, 2018

30th April, 2018

April - June, 2018

31st July, 2018

3. Due Dates for Other GST Returns Extended

|

Form No |

Applicable for |

Due Date |

|

GSTR 5 July-Dec |

Non Resident Taxable Person |

31 Jan 2018 |

|

GSTR 5A July-Dec |

Online information and database access or retrieval services |

31 Jan 2018 |

|

FORM GST ITC 01 July-Nov |

Taking GST Credit in Case of Existing Stock in Hand(Fresh Registration, Conversion of composition into Regular Scheme) |

31 Jan 2018 |

Reduction in Late fees for GST Return of Composition Dealer

Late fees for late filing of return for Composition Dealer has been made same as Regular Dealer

Late fees is as follows

|

Case |

Late Fees |

|

In case No Tax Payable |

20 per day |

|

In Case Tax Payable |

50 per day |

Note:-

Late fees Is to be divided equally into CGST and SGST

Even if IGST is payable, still for late fees we have to pay CGST and SGST(and not IGST)

No GST on Advance Received in Case of Goods

As per Time of Supply of Goods

Gst is payable on earlier of Invoice

Last Date of Invoice

Date of Payment

Hence, if payment received in advance, GST was payable on advance received

This condition has been removed now from 15 Nov 2017 vide Notification 66/2017

Hence, if advance received by Trader or Manufacturer, but goods not yet sold, now no GST is payable

However, receipt voucher is still to be issued by Trader/Manufacturer on receipt of advance(even though no tax is to be paid to govt)

Note:-

This concession is only for goods, not services Hence GST is payable if advance received by Service Provider

In case of Reverse Charge, if payment made in advance, still reverse charge is applicable for both gods and services.

Note:-

GST has had other changes. See GST Changes on the 10 November Meeting

Download in PDF

Changes Made in GST Council Meeting 6 Oct 2017

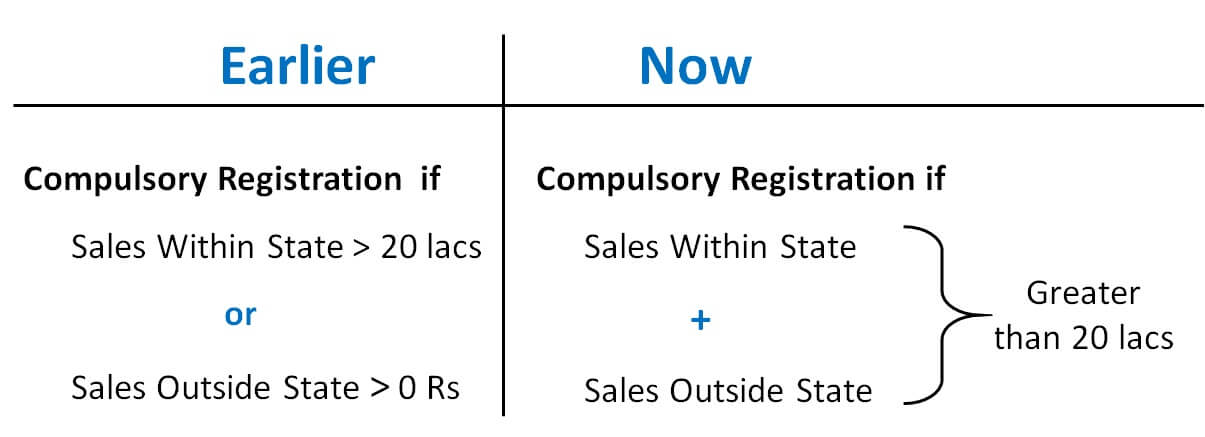

ViewRegistration Limit in GST is 20 lacs for Both Local and Interstate Sales

Earlier,

If a Person has turnover upto 20 lacs, they are not required to take registration

However if person is making interstate sales of even 1 Rupee, Compulsory Registration Required

Now,

If turnover is upto 20 lacs of Local + Interstate combined, then Registration Not Required

File Quarterly GST Returns 1, 2, 3

Earlier,

Normal Registered Dealer had to file Monthly GST Returns 1,2,3

Now,

If turnover is upto 1.5 Crores, then Quarterly Returns Required from Oct-Dec

However GSTR3B to be filed for Oct, Nov, Dec

Composition Dealer Turnover Limit Raised

Earlier

If turnover was upto 75 Lacs, then Person can Opt for Composition Scheme

Now

If turnover upto 100 lacs, then Composition Scheme can be availed

Option to Avail Composition Scheme

Person can opt for Composition Scheme till 31 March 2018

Suppose scheme opted in one month will be effective from Next Month

Example

Normal Dealer opts for Composition Scheme by 20 Nov 2017

He will file Composition Dealer Return and Tax starting from 1 Dec 2017

Reverse Charge to Unregistered Dealer suspended till 31-3-2018

Reverse Charge on purchases From Unregistered Dealer has been abolished till 31 March 2018.

Other Reverse Charge are still Applicable. like reverse charge on advocate and Good Transport Agency

However, what will happen to Reverse Charge already deposited is still not clear

Whether we can claim input of the same after payment or will it be refunded to us

No GST on Advance Received for Small Business

Suppose I receive money in advance in July

Sales made for the same in September

Tax on it was calculated in July Return to be paid by 20 Aug

Now

For small business(upto 1.5 crores)

Tax on it will be calculated in September Return to be paid by 20 Oct

This 1.5 Crores limit is of current year or last year is still not clear

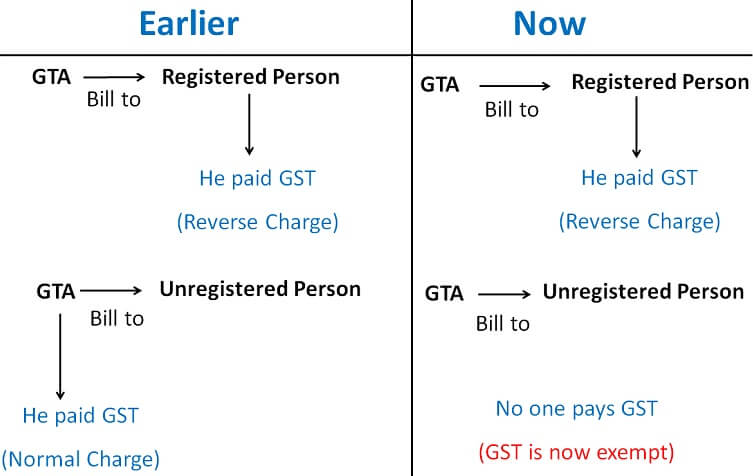

GTA Service To Unregistered Person Exempted

Earlier If Goods Transport Agency (GTA) provided services to Unregistered Persons, they had to pay GST

Because of this GTA were not willing to supply services to Unregistered persons.

Now,

This service has been exempted.

Other Changes

-

E-WAY BILL

Concept of E-Way Bill to be Introduced in Staggered Manner starting from 1 Jan 2018

There will be different dates for its launch in different states

In Whole of India,it will be launched by 1 April 2018

-

TDS TCS IN GST

TDS TCS in GST will also be differed to 1 April 2018

-

DUE DATES

Due Dates for GST Returns has been changed as follows

-

For Input Service Distributor

GST Return for July, Aug, Sep to be filed by 15 Nov 2017

-

For Composition Dealer

GST Return for July - Sep Quarter to be filed by 15 Nov 2017

-

For Input Service Distributor

-

Changes in Invoice Rules

For Certain Registered Persons, Invoice Rules will be changed

The details of same are still not been notified

Download Recent Changes in GST in PDF Format

Changes in Council meeting in 10th Jan

-

GST Council also approved levy of cess on intra State supply of goods and services within the State of Kerala at a rate not exceeding 1% for a period not exceeding 2 years.

-

The limit of annual turnover in the preceding financial year for availing composition scheme for goods shall be increased to Rs 1.5 crore. Special category States would decide, within one week, about the composition limit in their respective States.

-

Taxpayers under composition scheme will now need to file one annual return but payment of taxes would remain quarterly (along with a simple declaration)

-

There would be two threshold limits for exemption from registration and payment of GST for the suppliers of goods i.e. Rs 40 lakhs and Rs 20 lakhs. States would have an option to decide about one of the limits within a weeks’ time. However, the threshold for registration for service providers would continue to be Rs 20 lakhs and in case of Special category States Rs 10 lakh

-

A composition scheme shall be made available for suppliers of services (or mixed suppliers) with a tax rate of 6% (3% CGST + 3% SGST) having an annual turnover in preceding financial year upto Rs 50 lakhs. The said scheme shall also be applicable to both service providers as well as suppliers of goods and services, who are not eligible for the presently available composition scheme for goods.

-

Following matters were referred to Group of Ministers

i) Proposal of giving a composition scheme to boost the residential segment of the real estate sector.

ii) GST rate structure on lotteries.

- Changes made by CGST (Amendment) Act,2018, IGST (Amendment) Act, 2018, UTGST (Amendment) Act, 2018 and GST (Compensation to States) Amendment Act, 2018 along with amendments in CGST Rules, notifications and Circulars issued earlier and the corresponding changes in SGST Acts would be notified w.e.f. 01.02.2019.